Canada's instant payments era is starting

The RPAA is live. The RTR is coming. Canada’s payments landscape is about to be transformed.

Canada has long been an outlier among G7 economies: A sophisticated financial market without an instant payment rail. That is about to change.

The Real-Time Rail (RTR), Canada’s incoming instant payments scheme, represents a fundamental shift in payments infrastructure. Not an incremental upgrade, but a new operating environment with its own rules of participation.

Access requires registration under the Retail Payment Activities Act (RPAA), Canada’s new supervisory framework for payment service providers (PSPs). That establishes the compliance and operational baseline for any organisation seeking to participate. Banks, credit unions, and certain provincially regulated financial institutions are excluded, so aren’t required to register.

Under the act, PSPs don’t have a licence but are supervised by the Bank of Canada post-registration. RPAA registration is the legal prerequisite to performing covered retail payment activities.

This signals readiness. And regulators will treat it as such. Membership will be monitored, conditioned, and revoked.

Now, the RTR isn’t live yet, but the window to qualify is open. That means PSPs should already be working through RPAA registration, stress-testing their operations, and building institutional familiarity with the framework.

Waiting for a go-live date to begin that work is a strategic miscalculation.

So, the questions worth asking now are:

- How do the RTR and RPAA fit into your payments strategy?

- What does the path to registration look like for your organisation?

- Who will be the winners?

Let’s start with some context.

Real-Time Rail: where are we and what’s next?

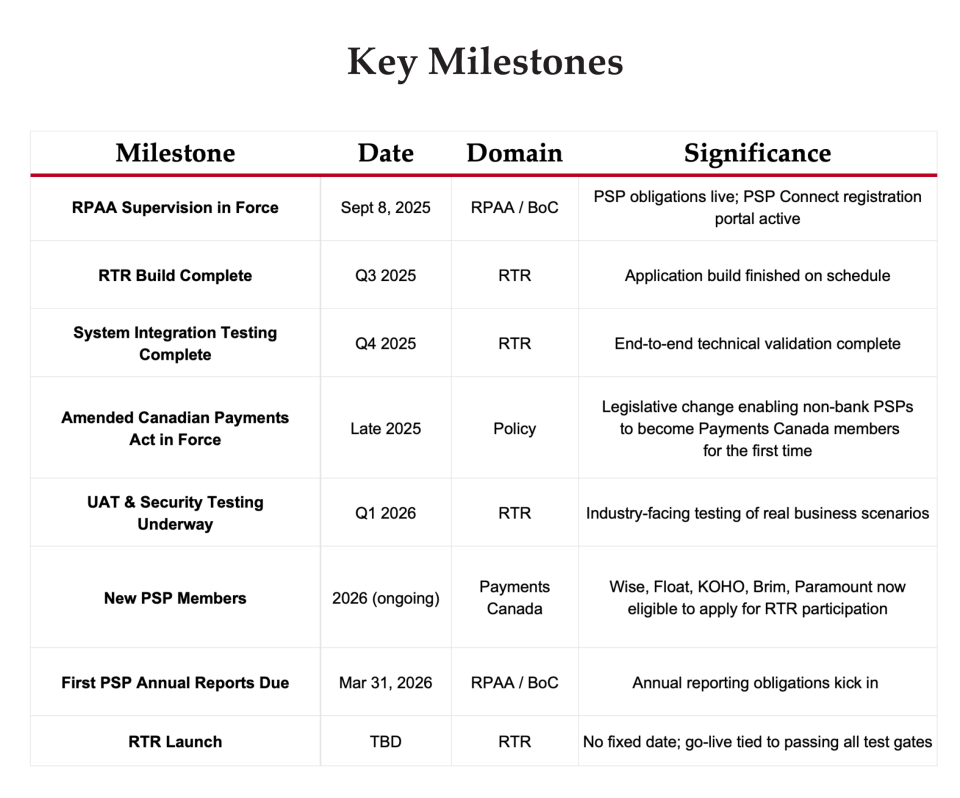

The RTR has cleared a major technical milestone.

Payments Canada has entered advanced testing, with participants engaged across multiple Software Development Life Cycle (SDLC) phases. Functional, performance, resilience, and security testing are actively underway, alongside operational readiness.

The programme will soon advance through a defined sequence of gated milestones: industry and participant testing, RTR Wave 1 participant certification and approvals, initial launch, and finally the migration of Interac e-Transfer.

Each phase represents a formal gate to production and conversion, with progression contingent on successful completion of each gate. Payments Canada will continue to provide the ecosystem information on progress through these gates and expects to announce a firm launch date for Wave 1 as the program progresses (widely expected to be in late 2026 and continuing into the first half of 2027).

Importantly, the RTR is not being built as a simple payment rail. Fraud controls — including a fraud scoring engine, Confirmation of Payee, and integrated fraud reporting — are included as core features from day one. That sets it apart from real-time payment systems in other markets. Many added similar controls only after launch.

The RTR will work alongside existing payment schemes like Interac e-Transfer (Canada’s broad, trusted peer-to-peer transfer service for consumer and small‑business payments), but with instant clearing and settlement, 24/7 availability, and richer ISO 20022 data. It expands what Canada’s digital payments layer can support. Together, these features bring Canadian payments firmly into the modern era. They open the door to more seamless, embedded payment experiences.

RPAA: what’s in force and why does it matter?

Meanwhile, the RPAA took effect on September 8, 2025. PSPs — including fintechs, e-money institutions, and non-bank payment firms — are now under formal Bank of Canada supervision for the first time. Registered PSPs are subject to enforceable obligations in two areas: managing operational risk, responding to incidents, and protecting customer money.

The Bank of Canada has published a public registry of PSPs, supervisory guidelines, and reporting expectations — creating a level of transparency and accountability that simply didn’t exist in the Canadian payments market before.

But RPAA is more than a ticket to the RTR. It is the foundational trust layer for the entire next chapter of Canadian payments — open banking, digital money, embedded finance, and beyond. Every party in those transactions needs to be confident that the others meet a basic standard of reliability and compliance. Trust has to be built into the infrastructure.

In each of these contexts, RPAA registration is not a simple compliance requirement. Far from it; this is a market credential. The PSPs that build genuinely robust frameworks, with auditable evidence and a track record of supervisory engagement, will be the preferred partners when banks, fintechs, and corporate treasuries are selecting who to connect with.

So don’t treat registration as a tick-box exercise. You should build genuinely resilient operating models or risk regulatory scrutiny and falling behind competitors as the market evolves.

How do the RTR and RPAA connect?

The relationship between RPAA and RTR is deliberate and structural. There is a clear sequence for PSPs to get ready:

- RPAA registration with the Bank of Canada — the trust and supervision baseline

- Payments Canada membership — formal access to participate directly in Canada’s core payment systems

- RTR application — including settlement account or Settlement Agent arrangement, technical certification, and rule attestation

5 steps PSPs must take now

The testing phase is not a waiting room. You must get started right away.

Step 1 — Anchor your strategy in RPAA compliance

Confirm your registration status and ensure your entity data (these are official details you must submit to the Bank of Canada when registering as a PSP. Things like your legal entity name, ownership and control information, and so on.) is current. Then move beyond registration to evidencing your frameworks: map your controls to the Bank of Canada’s published guidelines and build auditable records that would hold up under supervisory review.

Step 2 — Define your RTR access path

Decide whether direct or indirect participation is right for your business. Direct participation requires a settlement account and full technical certification; indirect participation routes through a direct participant. Both have different cost, control, and flexibility profiles. But an indirect participant does not clear or settle payments itself. It relies on a sponsoring direct participant to perform both clearing and settlement on its behalf.

Use the RTR Participation Guide to build a realistic sequencing plan.

Step 3 — Assess your operational impact

Review workflows, reconciliation, and 24/7 operational readiness. Ensure your technology supports ISO 20022 messaging and real-time fraud controls. Run simulations to identify gaps before go-live.

Step 4 — Prioritise early use cases

Not all payments carry the same risk in a real-time, irrevocable environment. Instant payroll, refunds, bill payments, and B2B payments with structured remittance data are natural first candidates.

Step 5 — Prepare your customers

Real-time, final, and irrevocable payments are important concepts customers need to understand before they encounter an issue. Update your terms and disclosures, strengthen your fraud education content, and ensure your support teams can accurately handle RTR-specific queries accurately.

How will PSPs gain a competitive edge?

Every PSP that connects to RTR will have the same underlying rail. Speed, 24/7 availability, and richer data will be table stakes. Just as internet connectivity stopped being a competitive advantage the moment it became ubiquitous, the same is true here.

Real differentiation will come from three sources:

- Speed of innovation: Institutions that can rapidly deploy embedded payment experiences — integrated into ERP systems, treasury platforms, and consumer applications — will capture value that infrastructure alone does not create. The rail enables; the experience differentiates.

- Trust architecture: RPAA supervision, combined with robust operational and fraud controls, creates a verifiable trust signal. In a world where banks, fintechs, and corporates are increasingly selective about which PSPs they integrate with, regulatory standing becomes a commercial asset. The PSPs that use RPAA as a genuine operating model upgrade — not just a registration exercise — will find doors open that remain closed to those that treated it as paperwork.

- Ecosystem positioning: The convergence of RTR, open banking write access, and emerging digital money frameworks creates the conditions for genuinely new financial products. PSPs that design for this convergence from the outset — rather than treating RTR as a standalone project — will be structurally better positioned.

The competitive edge will go to those who move fast on product, connect deeply across the ecosystem, and demonstrate the trust that access to critical infrastructure demands.

How RedCompass Labs can help

RedCompass Labs works with PSPs, financial institutions, and fintechs across Canada and globally to translate infrastructure moments like RTR into commercial and operational reality. Our experience spans all three of Canada’s core payment systems — Lynx (large-value), ACSS (batch), and RTR — and we bring global real-time rail expertise from markets where these journeys are already real.

RTR Operational Readiness Assessment

A structured assessment mapping your current state against RTR participation requirements across business, operational, regulatory, and technical dimensions. The output is a prioritised action plan, not a gap list.

AI-Powered Onboarding Navigation

We deploy our AI Onboarding Agent to help your teams navigate RTR’s rulebook, participation guide, and RPAA guidelines efficiently — compressing timelines and reducing rework.

Strategic Advisory

We can support you end‑to‑end — from helping to determine your access‑path strategy and settlement‑agent selection to 24/7 operating‑model design, fraud‑control architecture, and customer‑readiness planning. Tell us where you want to start.

If you need help with any of the above, get in touch.

Share this post

Written by

Neha Dasani

Payments Strategy & Delivery Lead, RedCompass Labs

Resources