Instant payments without borders: Nexus Global Payments

Nexus is a bold plan to connect the world’s instant payment systems. How will it work?

Today, instant payment systems operate at a national scale: fast within borders, yet fragmented between them.

But that may not be true for much longer.

Domestic instant payment systems are beginning to explore connectivity across jurisdictions, enabling cross-border payments in a matter of seconds.

That is, at least, the ambition behind Nexus: an initiative that spun out of the Bank for International Settlements (BIS) and set up in Singapore in March 2025.

If successful, Nexus will connect the world’s instant payment systems via a central framework, extending their many benefits to every corner of the globe.

So, what is Nexus? Will it work? And what does it mean for you?

What is Nexus?

Let’s start with the problem Nexus is trying to solve.

Cross-border payments are slower, more complex, and often more expensive than domestic alternatives, not to mention being more susceptible to fraudulent activity. A web of correspondent banks also means that each intermediary in the chain adds time, cost, and operational friction.

The issue is big enough that the G20 cross-border payments roadmap has been made a formal priority.

Now, there are multiple emerging approaches to solving this challenge, from stablecoins to wholesale CBDC experiments.

But Nexus takes a different route: building on the rapid expansion of domestic instant payment systems.

Its goal is to enable independently built instant payment schemes to communicate, translate, and settle seamlessly across countries. In other words, it wants to move money across borders as easily as it now moves domestically in markets like India or Europe.

Why do we need Nexus?

You might be thinking: instant payment schemes have already been linked. Why do we need Nexus?

And that’s a fair question.

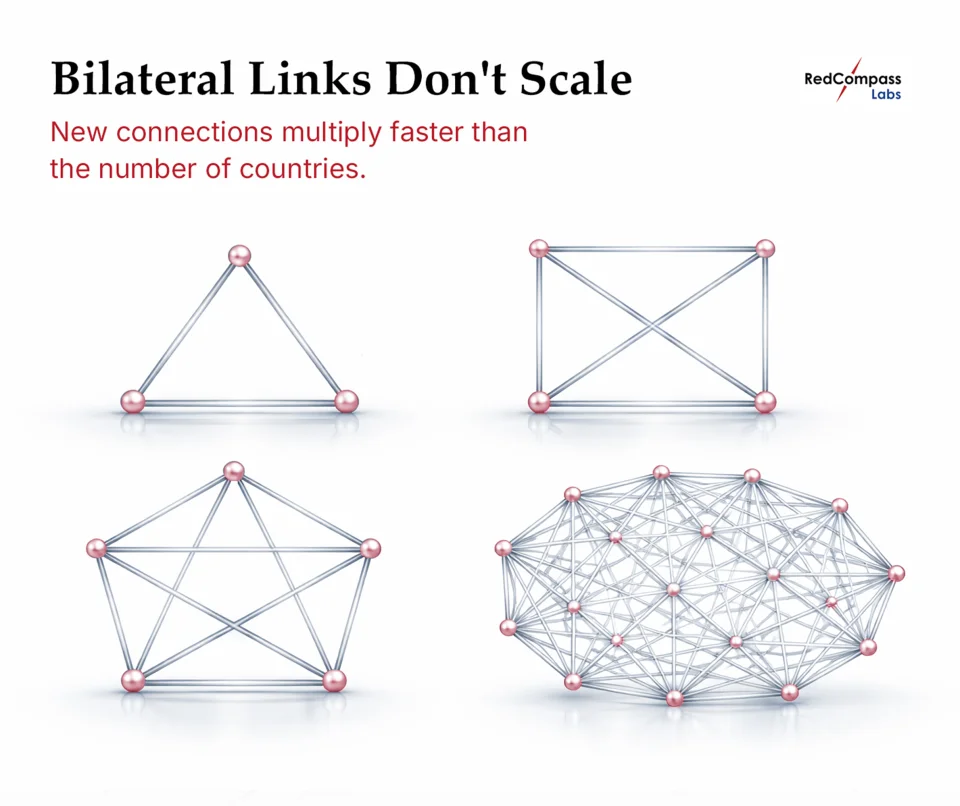

Through bilateral agreements, systems like PayNow (Singapore) are connected to UPI (India) and PromptPay (Thailand).

These corridors are valuable. But they are bespoke. Each bilateral connection requires tailored legal, FX, compliance, and operational arrangements. As more markets are added, complexity increases exponentially.

A scalable global model cannot rely on dozens of customized bilateral links. And that is where Nexus comes in.

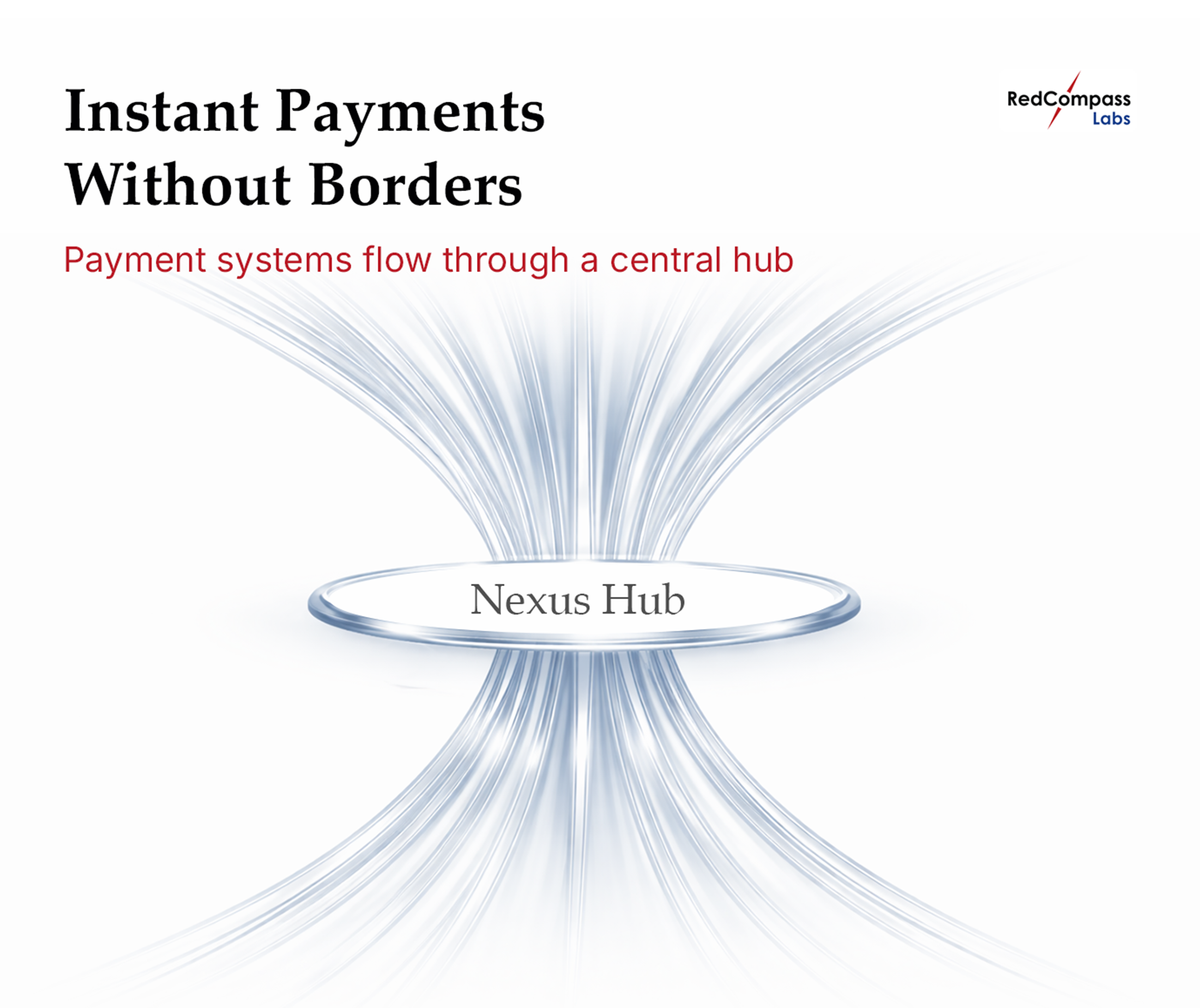

Nexus as a central hub

Nexus proposes a hub model.

Think of it like international aviation. It would be a logistical nightmare for every airport to operate direct flights to every destination worldwide. Instead, airports connect through hubs such as Heathrow or Dubai, providing access to hundreds of routes.

Under the Nexus model, each instant payment system connects once to a central framework, gaining access to all other connected systems. This makes everything much, much simpler.

Now, we’re not talking in hypotheticals: work has been happening in the background to solidify a proof of concept. Between 2021 and 2024, the BIS worked on Nexus with the central banks of Indonesia, Malaysia, the Philippines, Singapore, Thailand, India and the European Central Bank (ECB) to successfully prove that linking each country’s domestic instant payments systems via Nexus is possible and scalable.

We can expect to see updates on the legal and technical implementation during 2026.

But – and this will be particularly exciting for our European readers – the ECB has been in an exploratory phase since at least 2022, including proof-of-concept work involving Malaysia’s RPP, Singapore’s FAST and, in previous phases, the Eurosystem’s instant payments platform, TIPS.

The ECB’s involvement would be huge. 2.15 billion people live in India and the EU alone. That’s a quarter of the world’s population.

Nexus timeline

BIS communications indicate that Nexus is transitioning from blueprint toward structured implementation. This includes the development of a formal rulebook, technical implementation guides, and ISO 20022 specifications — overseen by a newly established managing entity, Nexus Global Payments.

Nexus Global Payments incorporated in 2025, by the founding central banks of India, Malaysia, the Philippines, Singapore and Thailand.

On the European side, the ECB’s involvement remains staged, with exploration and testing preceding any formal operational participation.

Will we see a Swift decline?

You may be wondering what this means for Swift. Since the 1970s, the Belgian-based secure financial messaging network has been the backbone of global cross-border payments. Nexus is challenging the status quo, but unlikely to spell the end for Swift.

Firstly, not every country has an instant payment system. So, Swift remains a vital service for international payments. However, the world is looking for a new way to facilitate cross-border payments. This means schemes like Nexus will force Swift to evolve, especially if it impacts revenue from low-value, high volume retail and corporate payments.

Swift may respond through collaboration, by developing its own competing solutions, or focusing more heavily on high-value payments, where instant payment systems often impose transaction limits.

Opening the gateway to scalable international payments

Nexus represents a blueprint for a more interoperable cross-border payments landscape. One that improves speed, cost, transparency, and access while leveraging existing domestic infrastructure.

Domestic instant payments systems have reset expectations of what modern payments look like for businesses and consumers. Nexus is the next chapter.

Want to know more?

We have decades of hands-on experience across instant and interoperable payments, from regulatory strategy and scheme participation to technical integration and operational readiness.

If you’d like to know more today, reach out to speak to our team.

Share this post

Written by

Anurag Bhole

Business Analyst, RedCompass Labs

Vishnu R Achuth

Business Analyst, RedCompass Labs

Resources