Open Finance: what you need to know

The FCA is hoping to deliver Open Finance in the UK by 2030. What’s changing?

If Open Banking was the warm-up, Open Finance is the main event. And the curtain has just gone up.

On 14 April 2026, the UK’s Financial Conduct Authority published its roadmap for Open Finance, setting out a clear path from vision to delivery by 2030. Consumers and businesses will soon be able to share their entire financial picture — mortgages, pensions, investments, insurance, credit — with any provider they choose.

For banks, this is not about compliance. It is about revenue, customer retention, and competitive strategy.

So, how is Open Finance different from Open Banking? And why should you care?

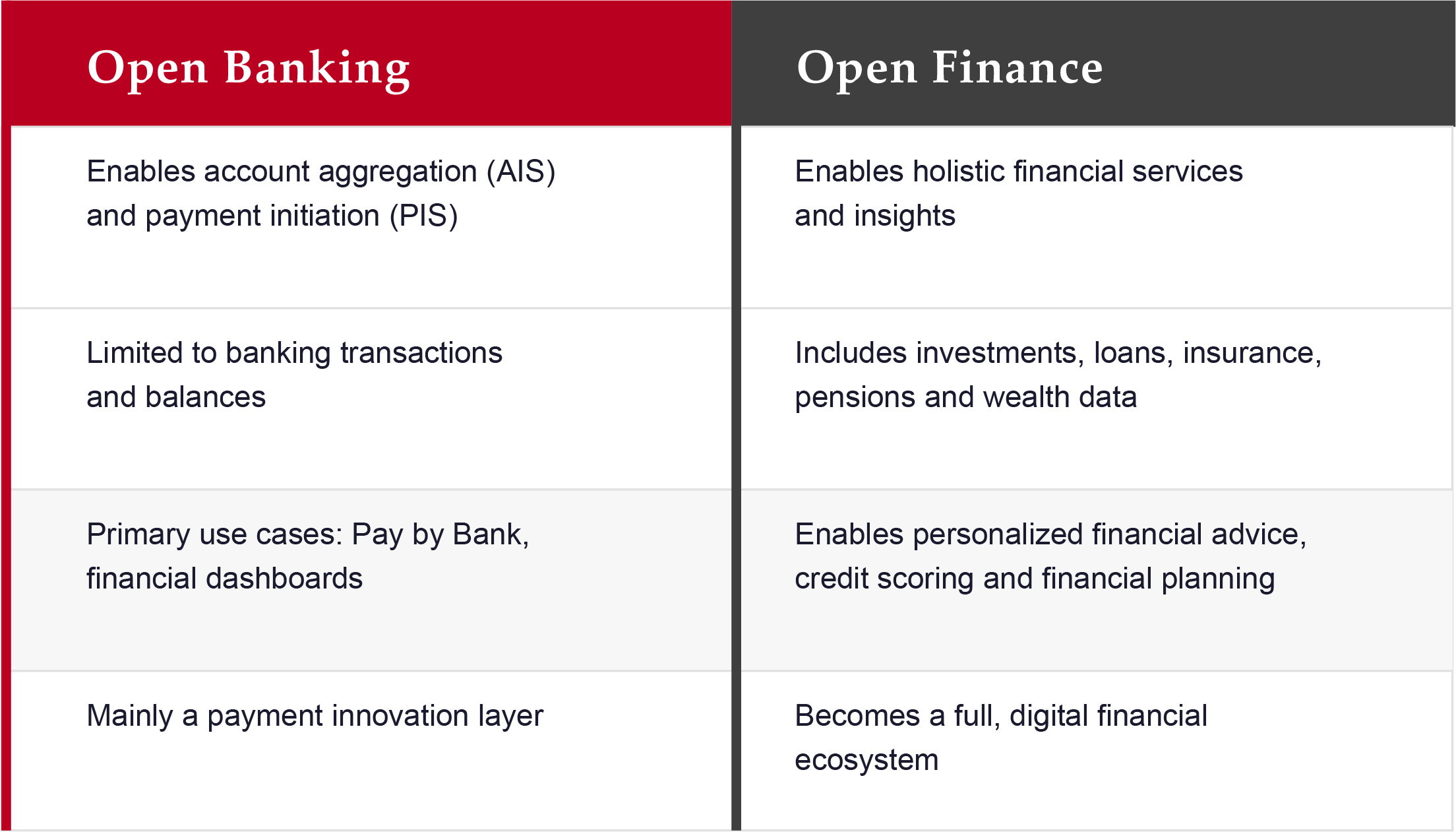

What is Open Finance in the UK?

The Open Banking regulation gave customers the ability to share their current account data and initiate payments from third-party apps. It found its footing. There are approximately 17 million active users, representing nearly 1 in 3 adults in the UK. The use cases — financial dashboards, Pay by Bank — are real and growing. But they remain narrow.

Open Banking touches one part of a customer’s financial life. Open Finance expands to all of it.

Where Open Banking cracked a window, Open Finance is like throwing open bifold patio doors. For the first time, a bank — and their competitors—will be able to see and act on a customer’s complete financial picture.

That is either a big opportunity or a big threat, depending on how prepared you are.

The FCA cites research by Open Banking Limited and EY suggesting the combined economic impact of Open Banking and Open Finance could reach £7.4 billion per year within five years. McKinsey estimates Open Finance alone could generate up to 1–1.5% of UK GDP by 2030.

That value will not be distributed evenly. It will flow toward institutions that have built the infrastructure, the partnerships and the products to capture it.

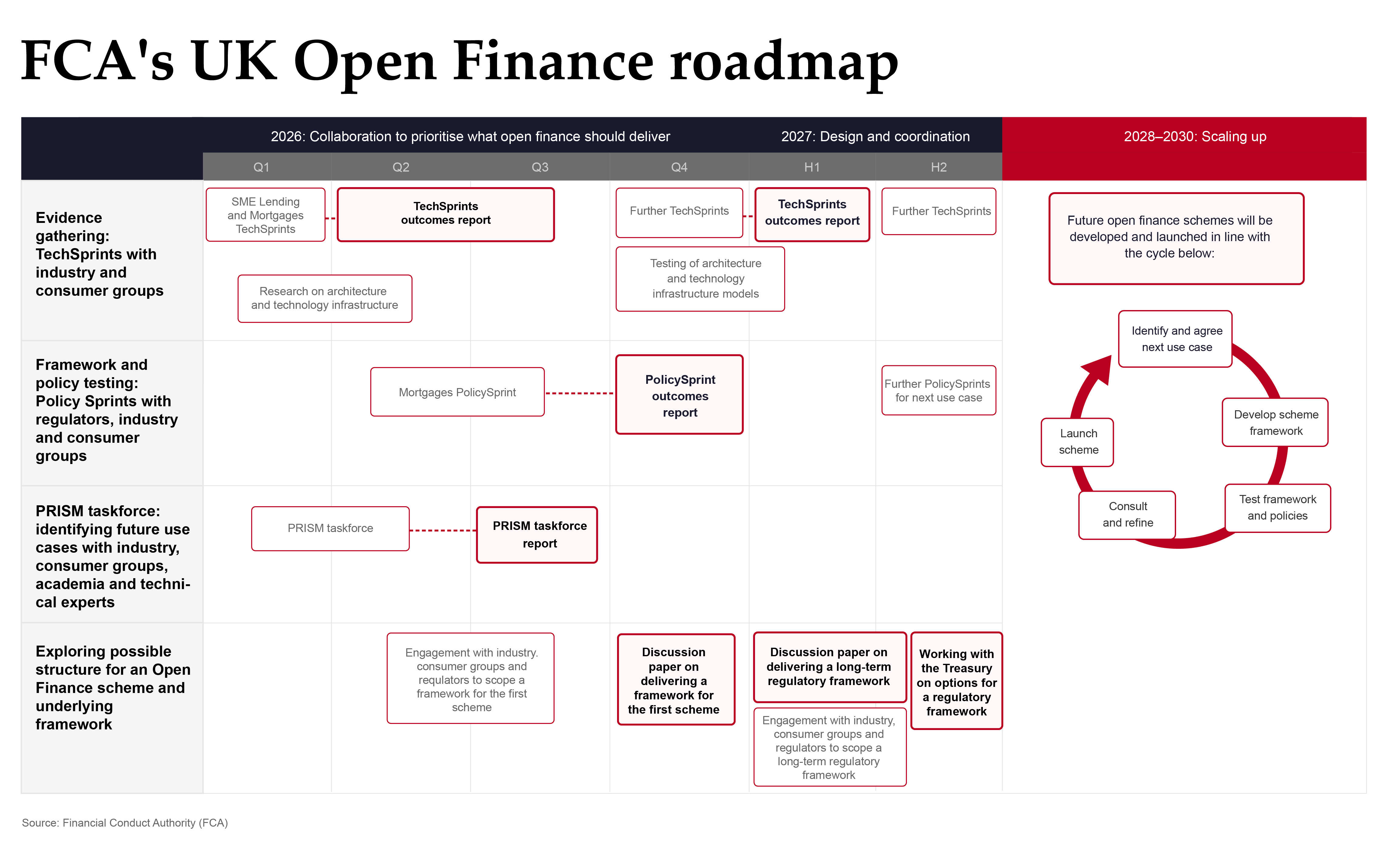

The regulatory timeline

The FCA’s roadmap sets out three formal phases:

2026 — Collaboration and prioritisation – The FCA is leading the development of Open Finance this year, working with financial institutions, consumer groups and fellow regulators to identify and prioritize high-impact use cases. The two priority areas are SME lending and mortgages.

Key milestones include a PolicySprint in Q2, a PRISM taskforce report by Q3, and a formal discussion paper on the first Open Finance scheme in Q4. The frameworks and use cases defined this year will shape the market for the rest of the decade. Banks that engage actively will help direct outcomes. Those that wait will inherit standards others shaped.

2027 — Framework design and coordination – The FCA will work with HM Treasury to develop options for the long-term regulatory framework for Open Finance. This is where the architecture of the regime gets built: governance structures, shared infrastructure requirements, and the regulatory underpinning for the first formal scheme.

2028–2030 — Scaling and delivery – Open Finance schemes are developed and launched on a rolling cycle: use case identified, framework designed, tested, consulted on, launched. The FCA has committed to reviewing priorities as markets evolve and new technologies emerge. By 2030, the expectation is a functioning, multi-scheme Open Finance ecosystem.

Click to enlarge

What does this mean for you and your customers?

Retail customers

The FCA’s roadmap sets out what Open Finance will deliver for consumers in practice. Its own case studies illustrate:

- Same-day credit decisions based on real-time financial data rather than static credit files

- Mortgage dashboards that draw on a customer’s current accounts, savings and mortgage data simultaneously, surfacing overpayment opportunities and switching options proactively

- Debt management tools that draw on every account to turn complex financial data into actionable insights, helping customers pay off debt faster

- Earlier identification of financial vulnerability — the FCA specifically cites gambling issues and financial difficulty as areas where broader data access enables proactive support before problems escalate

- Investment apps that conduct suitability assessments based on a whole-life view of finances, rather than the narrow snapshot available today

McKinsey has noted that customers increasingly want to see all their financial data in one place. Often from what they consider an independent party. The customer who can do that with one provider has very little reason to maintain relationships with five separate institutions.

Open Finance will accelerate consolidation of customer relationships. The question is whose platform they consolidate around.

SME customers

This is where Open Finance has the most immediate commercial potential for banks, and where the FCA has chosen to focus first.

Today, lending decisions for SMEs are based largely on static snapshots: last year’s accounts, a credit check, a conversation. The FCA’s own case study illustrates the problem directly; a small business rejected for loans because it could not provide adequate evidence of cashflow, despite being creditworthy. Open Finance changes this entirely.

With customer consent, a bank will be able to access real-time, comprehensive cashflow and financial data across all of a business’s accounts and products.

The FCA’s roadmap identifies the following as direct benefits:

- Lending approvals that were previously declined become possible with a fuller, more accurate picture of cashflow and business performance

- Loan applications pre-populated using reusable, portable data packages — reducing friction and documentation burden significantly

- Cash flow management tools built on real-time data helping SMEs spot shortfalls before they become crises

- More accurate credit profiling, enabling fairer and more precise lending decisions

For bank CFOs, the SME lending opportunity alone justifies serious investment in Open Finance readiness. The institutions that can offer faster, more accurate credit decisions — backed by richer data — will take market share from those still relying on annual accounts and relationship banker judgement.

Where’s the revenue opportunity?

Open Finance is not just a compliance cost. It is a new revenue layer and a competitive battleground.

Banks with well-designed APIs become infrastructure providers, not just product sellers. Those that invest in API quality now can charge for premium access and data enrichment services — there is growing precedent from Australia to the US.

Open Finance also expands the surface area for embedded finance, such as credit, insurance or pension products distributed inside a retailer’s app, an HR platform or an accountancy package.

McKinsey warns that banks which do not build these capabilities risk having their products distributed on someone else’s terms. And a bank that can see a customer’s mortgage, pension, investments and current account simultaneously can price more accurately, cross-sell more effectively and retain customers who would otherwise leave.

The FCA identifies fraud prevention and reduced financial crime as further outcomes — a fuller financial picture means better risk decisions, and that value compounds over time.

But the same data that creates opportunity creates threat. McKinsey believes that platform companies expanding into financial services target the distribution side of banking — historically 47% of global revenues and 65% of profits. The risk to banks is not a fintech building a better current account, it is a technology platform becoming the aggregation layer between your customers and their financial lives.

Oliver Wyman calls this “disintermediation from many fronts.” Banks that do not act strategically risk becoming interchangeable commodity suppliers.

How can you prepare for Open Finance?

The FCA’s roadmap sets out the timeline for scaling and delivery in 2028 – 2030, but banks can’t afford to sit tight and wait to see what use cases emerge. There’s an opportunity to both influence the direction of the regulations and ensure your own systems are ready for the next phase.

Immediate priorities (next 6 months)

- Engage with the FCA’s 2026 process – The Q2 PolicySprint and Q4 discussion paper — due later this year — are the primary opportunities to shape the regulatory framework before rules are drafted. The FCA has been clear on the need from input from stakeholders to shape the regulatory framework. That means senior voices, not delegation to compliance teams.

- Audit your current API infrastructure – Open Finance will require significantly more sophisticated financial data sharing capability than Open Banking. Understanding where your infrastructure stands now gives you time to make architectural decisions rather than emergency fixes when time is running out.

- Identify your highest-value Open Finance use cases – The FCA has started with SME lending and mortgages for good reason, there’s a large data gap and clear commercial opportunity for both. If either is relevant to your business, these should be your starting point.

The bottom line

Open Banking reached approximately 17 million active users — nearly 1 in 3 UK adults — by building on a relatively narrow data set covering payments and current accounts alone. Open Finance extends that to the entirety of a customer’s financial life. The value at stake, and the competitive risk, is proportionally larger.

The banks that will win are not necessarily the largest or the longest-established. They are the ones that treat Open Finance as a strategic priority rather than a regulatory obligation, that engage with the process while frameworks are still being shaped, and that build the data, API and ecosystem capabilities that will define distribution in the next decade.

The window (or bi-fold patio doors, if you’d rather) is open. The question is whether you walk through.

Get ahead of the Open Finance curve

Banks are in a strong position to capitalize on the myriad opportunities possible through Open Finance. Our experts can help you do that.

Whether you need help identifying immediate priorities or tackling longer-term projects such as boosting your data capabilities or building platforms and products, our experts have the experience and skills to help you at every step of the way.

Reach out and start a conversation today.

Share this post

Written by

Santhosh Kumar

Senior Business Analyst, RedCompass Labs

Resources