Open Banking and the Payments Forward Plan: What it means

UK Open Banking, Variable Recurring Payments, and the future of account-to-account payments now have a clear roadmap.

The UK started strong in Open Banking. It led early with the CMA (Competition and Markets Authority) Order and initial API standards. But momentum slowed over the years. Partly due to fragmented governance and a lack of a framework, other countries, like India, with UPI, have sped far ahead.

That is changing. The Payments Forward Plan, part of the UK’s National Payments Vision, brings clarity, central governance, and the establishment of a new Future Entity.

It puts Variable Recurring Payments at the fore. And it should help to speed up the adoption of Open Banking.

So, what’s happening? What does it mean for UK banks? And how can you prepare?

Forward thinking

Let’s start with the Payments Forward Plan itself.

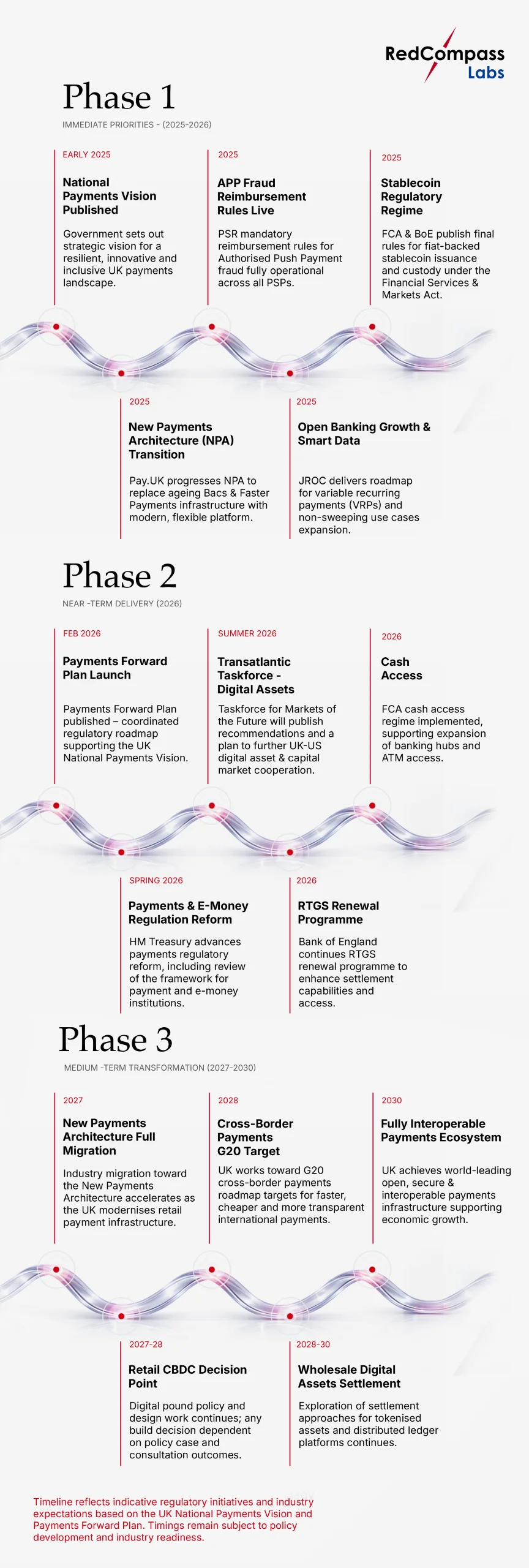

On 26 February 2026, the PVDC published its Payments Forward Plan. It provides a view of planned payments-related initiatives being delivered by the government and public authorities, and how each supports the delivery of the National Payments Vision. The plan brings together ongoing and upcoming work across retail payments, wholesale payments, and certain aspects of digital assets.

Banks that have been waiting to see which initiatives “win” — New Payments Architecture vs card, for example, or Open Banking vs proprietary apps, and digital assets vs traditional settlement — no longer have that luxury. The Forward Plan is a forcing function. The authorities have aligned, the timelines are set, and accountability is distributed across four regulators — HM Treasury (HMT), the Financial Conduct Authority (FCA), the Payment Systems Regulator (PSR), and the Bank of England (BoE) — who will each enforce their respective pieces.

The single most important thing about this document is not any individual milestone. It is the coordination architecture itself. Four regulators. One plan. Published jointly.

The UK’s Payments Forward Plan Timetable

How does that impact Open Banking?

For a long time, the Joint Regulatory Oversight Committee (JROC) attempted to steer the direction of Open Banking. But they struggled to deliver a clear, consistent, and scalable set of standards that the industry could rally behind.

This lack of clarity created friction and slowed adoption.

So, in Aug 2025, the Financial Conduct Authority (FCA) stepped in to take a more direct leadership role in shaping the future of Open Banking in the UK. With new legislative powers under the Data (Use and Access) Act, the FCA is now laying the groundwork for a more stable, long-term regulatory environment. One that can finally move the UK beyond interim arrangements and legacy structures.

The Payments Forward Plan now introduces a roadmap to get things done and the Future Entity, a dedicated body that will define and maintain the core technical and operational foundations for Open Banking going forward.

The Future Entity will serve as the primary standards setting body for Open Banking APIs. It will define the common, baseline technical and operational standards that all participants must follow, ensuring services remain interoperable, reliable, and consistent across the ecosystem.

It strengthens the UK’s ability to support innovation, scale new payment use cases like Variable Recurring Payments, and eventually pave the way towards Open Finance.

In April 2026, the industry will select an organisation to take forward the establishment of a body, and the Future Entity will be established in Q3/Q4 2026.

Why is this exciting?

Consider Variable Recurring Payments.

Variable Recurring Payments allow businesses to collect variable amounts on a recurring basis. An electricity company, for example, could trigger multiple account-to-account payments within pre-set limits. There’s no need for repeated Strong Customer Authentication (SCA). Just one agreement for prolonged authorisation. They’re instant, secure, cost-efficient, and purpose-built.

Variable Payments vs Direct Debits

Now, that sounds a little abstract, so here’s a little context.

Most people do not have the same energy bill for two months running.

It’s up in winter, down in summer. You never quite know what’s coming.

Right now, if you’re in the UK, you might pay by Direct Debit. Your supplier estimates your usage at the start of the year and sets a fixed monthly amount.

Some months you’re in credit. Others, you owe a catch-up lump sum you weren’t expecting. Every time your usage changes, your Direct Debit stays the same.

Card payments are an alternative. But they’re costly and vulnerable to fraud. (And they’re more effort for the consumer).

cVRP (Commercial Variable Recurring Payments) works differently.

With cVRP, you authorize your energy supplier once, through your banking app, with a monthly cap you set yourself. Every month, your supplier collects exactly what you owe, based on actual usage, at that quarter’s unit rate.

When the UK energy price cap drops in April, your bill drops automatically. When it rises in July, you pay the higher amount. But never more than your agreed limit, and never a penny more than you actually used.

The money moves instantly, and your supplier receives it the same day.

In a market where prices shift every three months and no one can predict what winter will bring, cVRP is a payment method that keeps up.

And it’s why the UK Payments Forward Plan has put Variable Recurring Payments front and centre.. It will have a major impact on UK businesses and consumers.

Two distinct flavours

- Sweeping VRP( “me-to-me” )

Automates transfers between a customer’s own accounts (e.g., current → savings).

Mandatory for the CMA9 banks since July 2022.

- Commercial VRP (non-sweeping)

Extends the same rails to pay external merchants or billers, and subscription management.

Participation is voluntary; pricing and liability are defined through bilateral or multilateral commercial agreements.

As part of the plan, industry owned, commercial schemes will run cVRPs.

The FCA says that, alongside the Future Entity, a competitive layer of industry-led commercial Open Banking schemes will operate above the core standards, including commercial VRP schemes. The FCA will also oversee the future ecosystem, including regulating the Future Entity and industry-led commercial schemes.

The first wave of cVRP will be implemented in Q1 2026. More use cases will follow in 2027.

Interface rules

If VRP is the use case, interface rules are what make it work at scale.

Without consistent, enforceable API standards underneath, account-to-account payments – including commercial VRP – cannot reliably reach across hundreds of banks. That is why the Forward Plan addresses both.

So, the proposed rules tackle persistent problems: inconsistent API performance, uneven reliability, and fragmentation across banks. This is what has prevented Open Banking from scaling beyond early data-sharing use cases.

They also clarify who does what. The FCA anchors regulatory oversight. The Future Entity sets technical standards. Innovation happens within competitive commercial schemes. That clarity gives banks and fintechs the certainty they need to invest and build toward account-to-account payments and, ultimately, Open Finance.

These rules are important because Open Banking relies on APIs that allow third-party providers to access bank data and initiate payments. Clear interface rules will help ensure standardised and secure API access, fair and non-discriminatory participation for fintech, and reliable technical performance across the ecosystem.

Ultimately, they will support a more sustainable and scalable Open Banking framework, enabling innovation in account-to-account payments and new financial services while maintaining strong consumer protection and operational resilience.

Consultation on long-term interface rules is planned for Q3 2026. A Policy Statement follows in Q1 2027.

How banks should start preparing

So, that’s what’s happening. What can you do to prepare?

You need to get ready for:

- API-first, real-time payments architecture to support account-to-account payments and VRPs at scale.

- New consent & mandate management for persistent, revocable permissions with limits and customer visibility

- Commercial readiness to support cVRP pricing, settlement, reconciliation, and sustainable Open Banking models

- Data platform modernization for real-time, event-driven, API-ready data supporting Open Finance and Smart Data

- API-native risk & fraud controls tailored for VRPs, real-time payments, and shared ecosystem accountability

Thinking about Open Banking?

Open Banking might seem like a challenge, especially as fintech firms enter the market with innovative solutions. But, as an established bank, you’re in a strong position to benefit from this shift.

Leverage your existing infrastructure and integrate APIs from other financial institutions, and banks can build services that connect merchants to multiple banks across the UK. This creates opportunities to deliver broader, more integrated financial solutions. Instead of treating fintech purely as competitors, banks can also collaborate with them to combine innovation with scale and trust. Such partnerships can help expand service offerings and keep banks competitive in an increasingly digital financial ecosystem.

If you’d like to learn more about Open Banking, speak to RedCompass Labs. We have helped banks get to grips with PSD2 and Open Banking in the UK. Our technology teams have extensive experience in APIs and interface design. Reach out to the team today.

Share this post

Written by

Ishwar Ahuja

Senior Business Analyst, RedCompass Labs

Santhosh Kumar

Senior Business Analyst, RedCompass Labs

Resources