Why 2026 is a make-or-break year for Pay by Bank in the UK

Amazon and eBay rolled out the payment service, but how can it become a mainstream option?

Something shifted in UK payments this year. In February, Amazon rolled out Pay by Bank, enabling 99% of its UK customers to use the payment method. Just over a week later eBay did the same.

The e-commerce sites join airline Ryanair, pizza delivery chain Papa Johns and takeaway delivery service Just Eat (among others) in offering their customers the payment option. This isn’t a brand-new method – Lastminute.com has been offering the option since 2018 – but backing from major e-commerce retailers signifies a new era.

The expansion demonstrates a broader shift to flexible account-to-account (A2A) payments becoming a feature of everyday transactions.

We’re a long way off this payment method matching (or eclipsing) tapping your card – only 6% of e-commerce transactions happened via A2A payments in 2025.

But regulations are helping to build momentum.

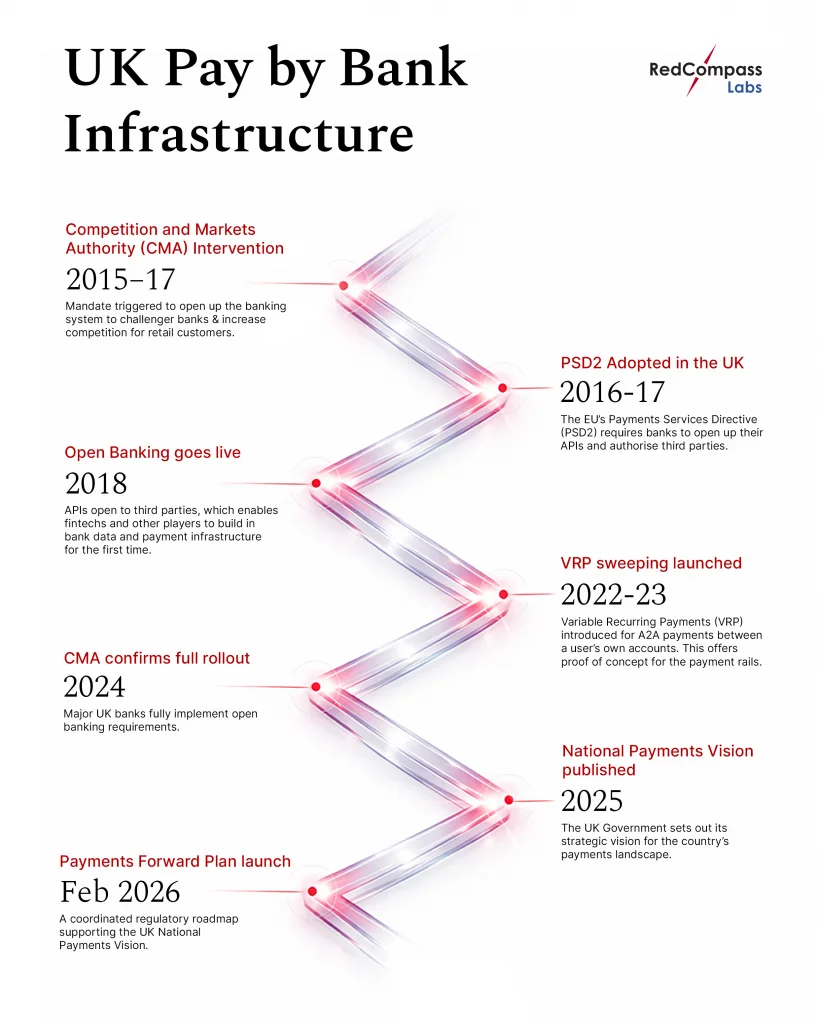

How we got here

The UK has taken a measured and deliberate route to arrive at this point in its payments modernization journey. Pay By Bank is a key feature of the UK’s wider Payments Forward Plan. This new vision prioritises payment innovation, increased competition and fraud reduction. Pay by Bank – as an account-to-account rails – advances all three.

At times, progress has mirrored that of European banks, but, unlike the EU, the UK has taken a regulatory-mandated approach. Instead of making the transition market-led, where European banks have been allowed to define their own API standards, the UK opted for competition driven with common, centrally-defined API standards.

Here’s how the infrastructure has been built up before Amazon and eBay’s Pay by Bank launch:

The UK’s financial ecosystem is more durable and interoperable thanks to this approach. It was deliberately slow and ensured all the correct pieces were in place when open banking launched.

Pay by Bank eliminates the Visa and Mastercard ‘tax’

Card payments dominate the landscape. Data from UK Finance shows that 64% of all transactions in the UK are card payments. And if cards are the dominant payment method, then Visa and Mastercard have absolute supremacy.

98% of UK card transactions are made via the two US card giants. Their business models depend on interchange fees, which merchants pay on every transaction.

Using Pay by Bank bypasses card rails entirely. It means no card networks or interchange fees. The money also moves direct from a customer’s bank account to a merchant’s, rather than the typical 1- 3 day cycle of card payments. The advantages of this can’t be underestimated for the working capital of larger merchants.

Merchants’ issues with card companies are best illustrated by Amazon threatening to stop accepting Visa credit card payments due to high transaction fees in 2021. Amazon argued that processing costs were an obstacle to providing lower prices. It’s easy to understand why they’ve launched Pay by Bank in the UK.

The uptake issue

Despite the developments in Open Banking payments over the past decade, consumer awareness hasn’t kept pace with the infrastructure.

Why? The simple answer is that UK payments already work really well. Contactless has been around since 2007 and became the post popular payment method in 2018. A lack of friction means consumers are not looking for a superior alternative.

An interesting comparison is India’s UPI and Pix in Brazil. Both are A2A payment rails which have seen huge adoption rates. The difference? Both systems are government-mandated, built to drive financial inclusion and benefit small businesses. By making the payments free at-the-point of use in countries with limited card access, the consumer motivation is clear.

Because the UK’s approach is regulatory and competition-driven, there’s no mandate, so banks have to give consumers a compelling reason to adopt Pay by Bank.

What could shift consumer behaviour?

- Merchant incentives: offering discounts or cashback for offering Pay by Bank

- Reduce friction: Pay by Bank UX requires more steps than a card tap, it’s important to close that gap

- Build trust: Consumers needs to be confident that if something goes wrong – accidental payment, disputed transaction – they have recourse. Chargeback capabilities are essential

- Familiarity: When more major platforms offer the payment method, it becomes more habitual

How to unlock scale: Variable Recurring Payments (VRP)

A VRP is a more flexible version of a direct debit, that’s built on open banking rails. It allows merchants or services to take payments from a bank account, but unlike direct debits, which are for a set amount, a VRP (as the name suggests) varies from payment to payment.

(for a more comprehensive explainer of how VRPs work, we have a great one here)

At the moment, VRPs are limited to what’s called “account sweeping”, where consumers can move money between their own accounts. Where this could really help to scale Pay by Bank is for cVRPs (commercial Variable Recurring Payments) which can be used for subscriptions, utilities or instalment payments. They are flexible, instant and ideal for repeat purchases, not just single transactions.

The first wave, targeting these use cases, is due for roll out in early 2026 (i.e. around now) with the foundations being laid for phase 2, where e-commerce payments would come into play.

While we may be waiting at least 12-18 months for phase two, the implications are clear; cVRP can offer greater customer experience than direct debits. And it can support the UK’s payment vision for increased competition and innovation.

A strategic challenge for Visa and Mastercard

UK bank bosses are working on building an alternative to the US card giants. Whether this is a new card system, a more concerted push for A2A payments, or both, the direction of travel is clear – build an everyday payment mechanism that competes with Visa and Mastercard at the checkout (both online and POS).

If we take UPI as a yardstick for A2A adoption, India has seen a dramatic reduction in card network market since its launch. With the UK’s payments vision prioritising A2A payments as a strategic goal, we are likely to see a challenge to card dominance and open banking evolving from a data-sharing network to an everyday payment solution.

It’s important to stress that Visa and Mastercard are not standing still. In the last few years Visa has acquired Tink, while Mastercard did the same with Aiia, demonstrating the shift towards in open banking and A2A infrastructure as a viable payment option.

How Pay by Bank becomes mainstream in 2026

It’s a make-or-break year for the UK payments ecosystem. Major players like Amazon and eBay launching Pay by Bank will accelerate consumer awareness, but that alone is unlikely to significantly tip the scales.

We’re not predicting 2026 is the year that it succeeds or fails, but what happens will determine the trajectory for the next 5 years.

What needs to go right:

- Commercial VRP delivered and rolled out on schedule

- Regulatory frameworks continue to support A2A payments with clear consumer protection rules

- More major platforms follow Amazon and eBay’s lead – both e-commerce and in-person retail

- Increased awareness and incentives for consumers and merchants

The window for the rise of Pay by Bank is open but won’t remain so indefinitely. We’re likely to see higher adoption rates in e-commerce, as demonstrated by Amazon and eBay. A change in consumer habits and improved UX is necessary for a shift in how people pay at the supermarket or other retail stores. It will be a longer journey to get there.

Amazon and eBay’s launches need to be a catalyst for Pay by Bank or it will remain a promising open banking capability that never fulfilled its potential.

Thinking about Open Banking?

Open Banking might seem like a challenge, especially as fintech firms enter the market with innovative solutions. But, as an established bank, you’re in a strong position to benefit from this shift.

Leverage your existing infrastructure and integrate APIs from other financial institutions, and banks can build services that connect merchants to multiple banks across the UK. This creates opportunities to deliver broader, more integrated financial solutions. Instead of treating fintech purely as competitors, banks can also collaborate with them to combine innovation with scale and trust. Such partnerships can help expand service offerings and keep banks competitive in an increasingly digital financial ecosystem.

If you’d like to learn more about Open Banking, speak to RedCompass Labs. We have helped banks get to grips with PSD2 and Open Banking in the UK. Our technology teams have extensive experience in APIs and interface design. Reach out to the team today.

Share this post

Written by

Pratiksha Pathak

SVP, Head of Payments, RedCompass Labs

Resources