ISO 20022 is arriving all at once

Fedwire, CHIPS, and Swift (CBPR+) are all moving on essentially the same timeline. What do US banks need to do?

2026 is another major year for ISO 20022. And no country is under more pressure than the United States.

For the first time, Fedwire, CHIPS, and Swift (CBPR+) — the core clearing systems that move large-value and cross-border payments in the US— are all changing messaging standards essentially on the same timeline. There are hard cut-over dates and limited fallback options. This isn’t a phased migration like previous years.

US banks will be forced to confront decades of accumulated technical debt in their payments infrastructure. Getting ready requires global coordination, multiple critical payment rails, strict cut-over dates, and permanent changes to data models.

That means it’s going to be a lot of work.

If you haven’t started getting ready, there’s still time, but the deadlines will come quickly. Here’s how you can prepare.

ISO ISO baby

By November 2026, the three payment systems that sit at the centre of US large-value and cross-border payments —Fedwire, CHIPS, and SWIFT—will all be operating exclusively on ISO 20022. This means the formats that banks have been using to send and receive messages for decades will no longer be accepted. If a payment doesn’t meet the new standards, it will fail.

What makes this transition unusually difficult is timing. All three networks converge in a single month. There is no opportunity to stagger the effort, complete one migration, stabilize, and then move on to the next. Instead, banks have to prepare upstream and downstream systems. That includes (but is not limited to):

- data models

- sanctions screening and fraud

- investigations

- reconciliation

- middleware

- liquidity processes, and

- customer channels & communications.

A weakness in one rail or data element can disrupt multiple payment flows. If a bank cannot reliably send or receive Fedwire payments — even briefly — it becomes hard for them to move large sums of money for other payment types like CHIPS. This includes funding their settlement account at the Federal Reserve Bank. What begins as a data-format issue becomes an operational and liquidity issue.

What is Changing with Fedwire, CHIPS, and Swift (CBPR+)?

Fedwire, CHIPS, and Swift are all making essentially the same shift. This includes the move to structured (and hybrid) addresses and changes to exceptions and investigations handling. There are, however, important differences in how each scheme implements these changes.

Fedwire Funds Service

The transition away from legacy formats happened in July 2025.

The November 2026 milestone is an upgrade of the existing ISO 20022 implementation.

One of the most disruptive changes is how addresses are handled. Historically, addresses could be passed as long blocks of free text, often copied from legacy systems or customer input with minimal validation. Under the new rules, every address must contain specific structured elements, supplemented by only two short free-text lines. Fully unstructured addresses will fail validation and be rejected. This pushes data-quality requirements upstream into client onboarding, payment channels, and internal reference data.

In November, Fedwire is also aligning its exceptions and investigation implementation with the 10 frequent investigation use cases defined by Swift.

CHIPS® ISO 20022

CHIPS is intentionally aligning its ISO 20022 implementation with Fedwire. The message types, core data elements, and overall structure closely mirror Fedwire’s approach, with only limited CHIPS-specific code lists and conventions.

This reduces complexity at a design level, but it also raises the stakes. If your internal data model or validation logic is wrong, the same defect can affect both Fedwire and CHIPS processing at the same time.

Swift CBPR+ (SR 2026)

Swift’s Standards Release 2026 (SR2026) is the most consequential phase of the CBPR+ migration to ISO 20022. From 14th November 2026, banks must originate and process native ISO 20022 (MX) messages under much tighter usage and validation rules. Most MT (Message Type) dependencies and transitional flexibilities will be effectively removed or chargeable.

SR2026 introduces new versions of core CBPR+ payment and investigation messages. It mandates the use of structured or hybrid postal addresses and hardens Business Application Header requirements. The new message standards also expand network-level validation of identifiers, code sets, and mandatory fields.

Some checks may initially operate in a non-blocking model (i.e., payments proceed while flagging data-quality issues). But message quality and data completeness will be enforced more strictly at the network level.

For banks, this work elevates ISO 20022 readiness from a technical mapping exercise to an operational and data-quality imperative. The new regulations require changes across payment engines, screening systems, investigation workflows, and front-to-back operating processes ahead of the November 2026 cut-over.

Other Format and Screening Implications

ISO 20022 messages carry far more structured data than legacy formats. Unique transaction identifiers, explicit payment purpose codes, and detailed remittance information are now standard rather than optional. This has clear benefits, but it also means sanctions screening, and AML systems must be capable of parsing and analysing XML content across many more fields.

Banks also need to ensure that character-set enforcement does not unintentionally block legitimate payments. Systems that silently normalised or truncated data in the past can now cause rejections.

How does ISO 20022 impact regulations and policy?

The regulatory impact of the ISO 20022 migration goes beyond technical compliance. Fedwire’s operating rules are being updated to reflect the mandatory use of ISO 20022, meaning that sending a non-conforming message can constitute a breach of network rules, not just a processing error.

From a financial crime perspective, ISO 20022 explicitly carries the information required under the U.S. Travel Rule. Regulators will expect banks to retain, screen, and produce this data consistently. Structured party data also increases expectations around OFAC screening, particularly with respect to ownership rules and name matching.

Legal frameworks such as Regulation J and UCC Article 4A continue to govern payment finality, but internal procedures must now reflect new message types and flows. At the same time, XML gateways and APIs introduced as part of ISO 20022 implementations fall within the scope of SWIFT’s Customer Security Controls and must be tested and secured accordingly.

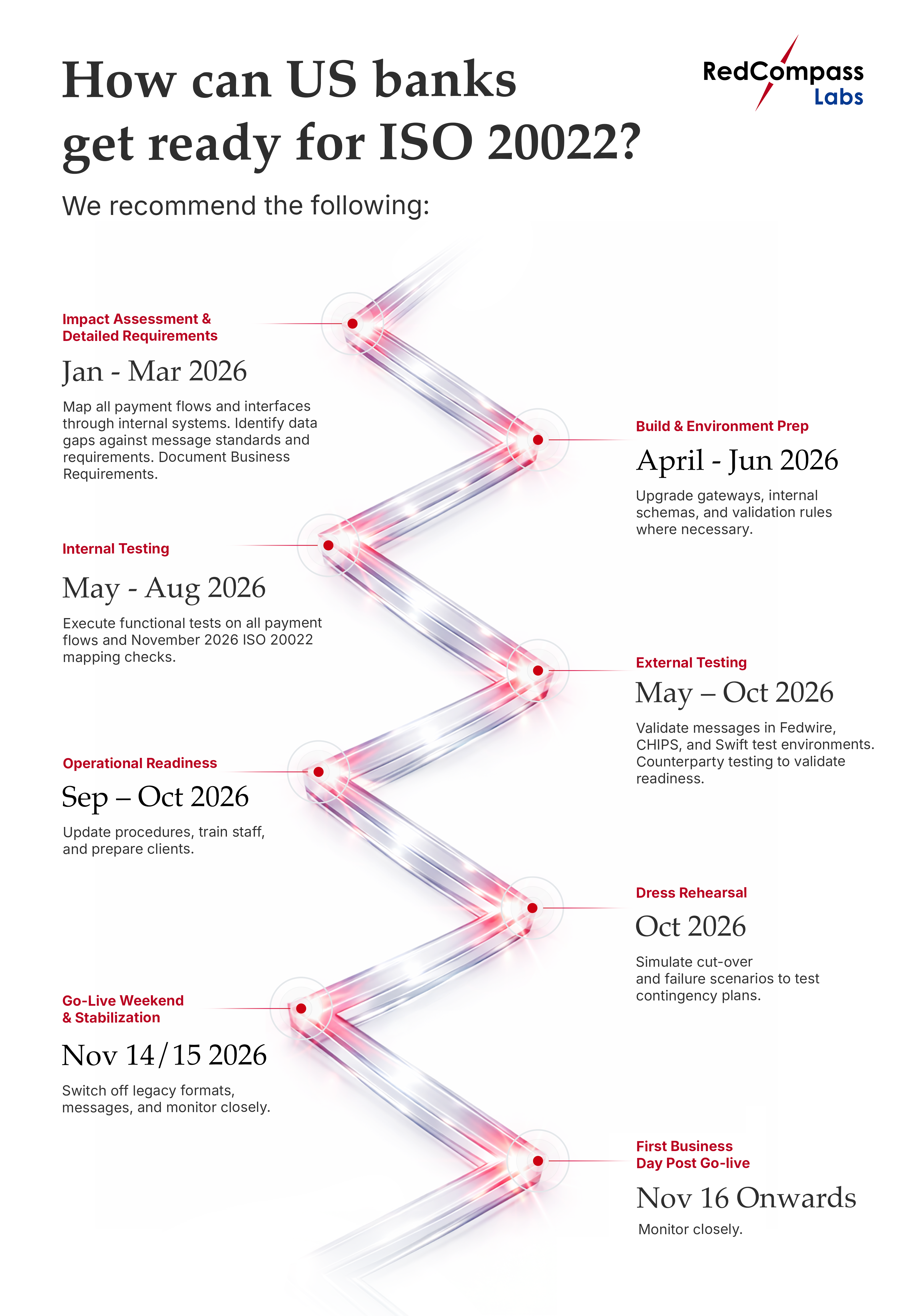

Key ISO 20022 Milestones to November 2026

What this timeline really shows is how little slack exists.

The technical build is the visible part of the work, but it’s not the biggest obstacle around ISO 20022. The real challenge lies with operational and change management. Operations, compliance, and customer-facing teams need time to learn new data standards, interpret new error messages, and operate redesigned investigation processes. Organisations that treat the new rules as an afterthought—rather than a core workstream—will likely discover significant operational challenges at go-live.

Tip of the ISOberg

This is one of the most significant changes ever imposed on U.S. payment infrastructure. What makes this different from earlier programmes is not just its scope, but the fact that these changes are all happening at once. So, your preparation should begin with targeted readiness assessments to pinpoint where legacy formats, internal data models, and interfaces fall short of the 2026 requirements. From there, you must implement tooling. This needs to reliably convert and validate messages, enforce character-set and data-quality rules. And, it’s got to support automated testing across Fedwire, CHIPS, and SWIFT environments.

In parallel, your compliance functions need enhanced sanctions and AML screening capabilities. This is to ensure that richer, more structured data actually improves detection (rather than introduces new gaps).

Your programme should conclude with disciplined governance, cut-over execution, and post-go-live optimization, enabling institutions to stabilize quickly and realize lasting value.

This is about data structure, data quality, and regulatory transparency.

Need help?

We’ve decades of hands-on experience across ISO 20022 programmes globally. We bring deep, practical expertise to help you navigate the technical and regulatory requirements, as well as the operational, data, and change-management challenges inherent in large-scale payment transformations. Please reach out to the team to talk through.

Share this post

Written by

Kellie Johnson

SVP, Payments, Americas, RedCompass Labs

Resources