FedNow vs RTP: Can two real-time payments systems coexist in the US market?

We’ve seen this dance before in Europe.

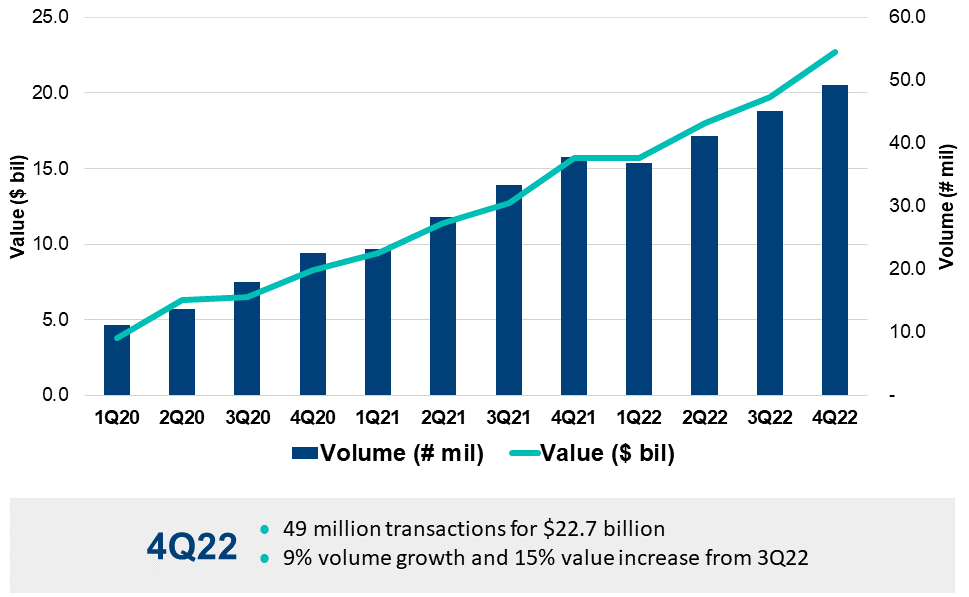

In November of 2017, The Clearing House’s RTP network processed the first real-time payments in the United States and has since continued to grow. Today, it has more than 280 participants capable of sending and receiving real-time payments. The system, which supports both payer-initiated payments as well as request-for-payment initiated payments, has seen steady growth, and processed over 45 million transactions for a total value of close to $20 billion USD in the third quarter of 2022.

However, there’s a new kid on the block. The Federal Reserve Bank, after flirting with the idea for many years, is finally in the process of launching a competing real-time payments solution, FedNow. The service, which will also support request-for-payment, is scheduled to go live in 2023, and is currently being piloted by about 100 financial institutions.

How do the systems compare?

In terms of fees, both systems will be equivalent at 4.5 cents per originated transaction, so there is no clear price advantage for either solution. They support similar use cases, including B2B, B2C, and P2P. When it comes to transaction amounts, FedNow has set a lower transaction limit of $500,000 instead of RTP’s $1 million.

The main difference between the systems lies in their governance: whereas RTP is operated by a consortium of large banks, FedNow is operated by the Federal Reserve Bank. This can give FedNow an edge over RTP, as the system will allow for intelligent liquidity management, allowing banks to transfer funds between their FedNow account and their Federal Reserve master account.

RTP, on the other hand, has an edge when it comes to interoperability: the popular P2P payment service, Zelle, can use RTP to settle payments, and The Clearing House (TCH) has participated in cross-border initiatives such as Immediate Cross-Border Payments (IXB).

Additionally, RTP has developed value-added services for its members, such as the ability to attach PDF or XML documents to payment requests, and account number tokenisation.

You mentioned Europe?

In Europe, we’ve seen a similar competition between different market infrastructures capable of processing SEPA instant credit transfers. EBA Clearing, which could be seen as the European equivalent of The Clearing House, launched its RT1 service in April 2016 with an official go-live in November 2017.

Following this, and much like the Fed now, The European Central Bank entered the instant payments party fashionably late in November 2018 with the Target Instant Payments Settlement service (TIPS). However, with a significant number of banks having already joined RT1 or domestic instant payment clearings, TIPS initially had little traction for the service, despite coming in with aggressive pricing.

In order to increase their market share in instant payments, just like the Federal Reserve’s recent announcement of initial fee cuts for FedNow, the European Central Bank also took a number of measures:

- They moved instant payments settlement out of Target2, the European Real Time Gross Settlement mechanism, into TIPS.

- They required each bank that was offering Instant Payments to have an account at TIPS (which meant they would need to be able to receive instant payments on that account).

- They allowed other European clearing houses to instruct TIPS instant payments on behalf of their customers, allowing banks to use their RT1 connectivity to send and receive payments within the Eurosystem.

- They introduced a contentious transaction-based charge for other clearing houses to use TIPS settlement, thereby artificially inflating the prices of the clearing houses competing with TIPS by as much as 25%.

- They introduced automated liquidity management between a bank’s Main Cash Account (where they are required to maintain their reserves) and their TIPS account. This is scheduled to go live with the consolidated Target platform in March 2023.

Unfair you say? Despite the increasing popularity of the ECB’s TIPS platform, the private sector equivalent RT1, as well as the domestic schemes, continue to exist and to thrive. They have done so through the development of innovative services such as Request to Pay and by keeping their costs low, all benefitting European payment users.

Does that mean both systems will continue to co-exist in the US Market?

We would hope that competition between TCH and the Fed will continue to not only push innovation forwards, but also to create a downwards pressure on pricing. And there certainly is the ability for prices to come down: an Instant payment in Europe costs banks 0.2 cents, less than a 20th of the equivalent cost in the USA. The Fed slashing fees for banks participating in FedNow for the first few months is a shot across RTP’s bow and could potentially trigger a first cut in prices from The Clearing House.

Based on our experience in Europe, we would say that it is likely that both systems will continue to flourish in the US market.

This means that banks will need to continue to decide which system they wish to maintain. Maintaining both will lead to additional costs for payment service providers. Interoperability will remain a challenge, as the instant settlement component of real-time payments renders message exchange interoperability a true challenge.

Share this post

Written by

RedCompass Labs