Can Europe cope without Visa and Mastercard?

The EU is building payment solutions to rival Visa and Mastercard’s dominance – the next step is getting consumers to adopt them.

Updated: February 2026

In 2020, we wrote a blog titled: Can EU banks compete with Visa and Mastercard?

At the time, the EU recognized the growing prominence of account-to-account (A2A) rails, instant payments and open banking. Europe already had strong domestic payment schemes and systems in countries like France, Germany and Belgium, but their capabilities didn’t extend to cross-border payments across Europe. So, the European Payments Initiative (EPI) was announced.

16 Tier-1 banks set out with the ambitious goal of creating European payment system that could rival Visa and Mastercard, as well as meeting the threat from tech giants such as Alipay and Google head on.

Building this infrastructure made sense in 2020 and the initiative began as a push for innovation.

Six years later, the political climate has shifted. The US has spooked its allies and created legitimate concerns around relying on the American card giants. What started as a push for sovereignty has become need to maintain the security of a continent’s payment rails.

Europe has built the infrastructure. SEPA (Single Euro Payments Area) Instant payments is live, and Wero has over 47 million users.

The big question; If there’s a viable alternative to Visa and Mastercard, what would it take for consumers to use it?

Why the urgency for EU-operated payments has grown

In 2020, the desire for European payment alternatives was driven by innovation and competition. The EU wanted more choice and lower costs (for merchants and consumers) using modern payment technology. These arguments still stand but what’s shifted is the urgency behind them.

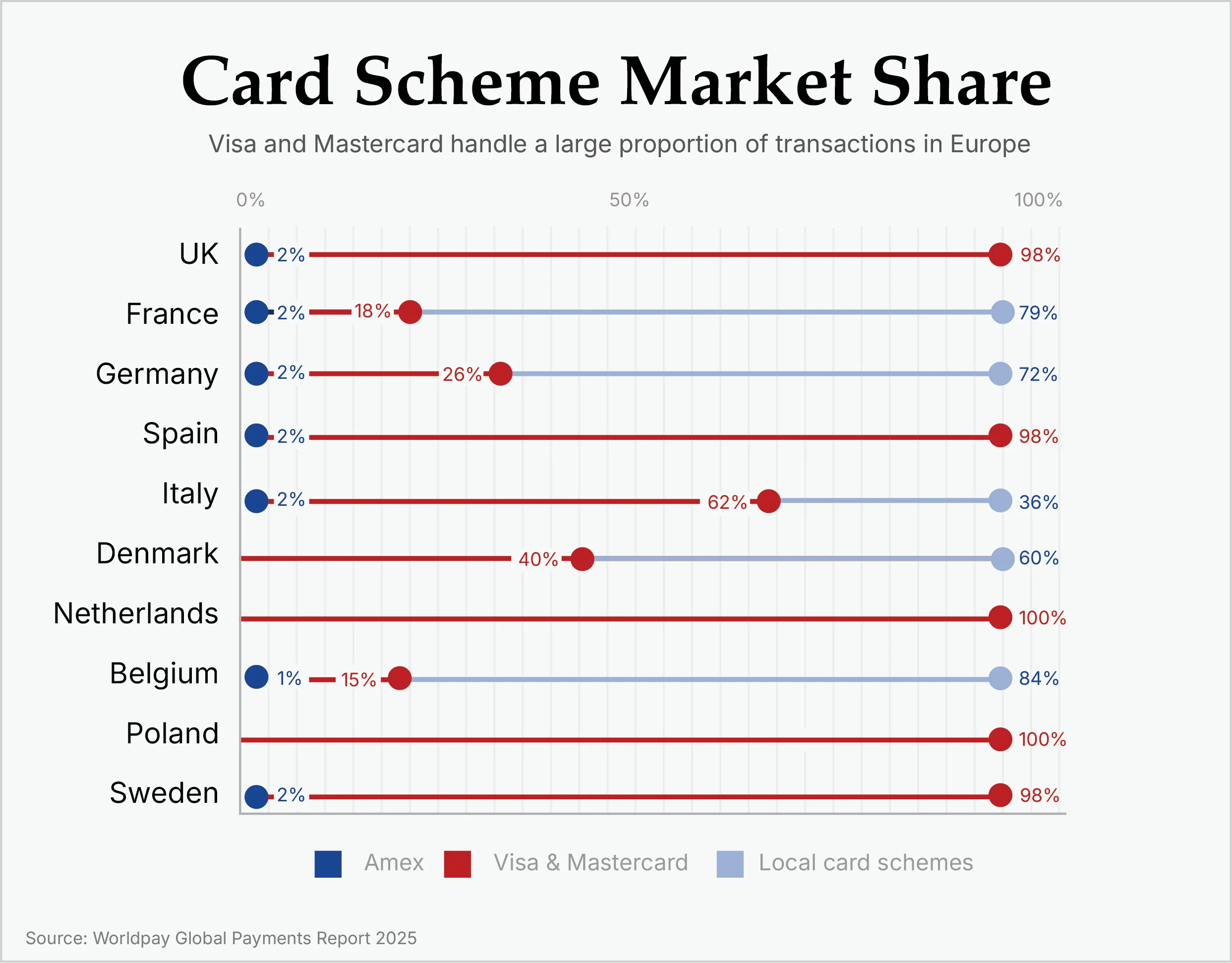

The UK and countries in the EU like Spain, the Netherlands and Portugal, are still heavily reliant on Visa and Mastercard. This wasn’t an issue when the EPI was launched, but it’s not 2020 anymore and now there’s a necessity to offer a viable alternative.

The ECB’s data shows that 66% of Euro area card transactions happen via international card schemes. It’s a similar story with processing layers and partner networks. There are significant risks that come with critical payment processing infrastructure depending entirely on companies outside of Europe, so the EU needs more resilience in its financial system.

It’s not unthinkable that Europe’s payment infrastructure could be put at risk by an unexpected shift in geopolitical pressure. It’s vital there’s a solution in place which ensures EU’s financial institutions are still in control of its payment systems.

Did EU banks choose the right battlefield?

One of the key pillars set out in the EU’s retail payments strategy in 2020 was to reduce dependency on US card networks. The original blog questioned whether it was the right time to challenge Visa and Mastercard’s dominance, or even the correct fight at all.

Visa and Mastercard had a resilient and ever-present payment system, so it made sense to focus on electronic payments. A viable alternative to the Visa/Mastercard duopoly was leveraging SEPA, SEPA Instant and Open Banking, to build something different for consumers and businesses.

This is the path that the EPI eventually took, but more by circumstance than design. Several of the founding members withdrew and the scope narrowed. No more card offering. Instead, there was a pivot to an account-to-account model, using SEPA Instant Credit Transfer (SCT Inst) and Wero, a digital payment wallet launched in 2024.

So, the switch in focus was the right call, because the challenge has changed. The EPI isn’t trying to get a foothold in the world of card transactions; its mission is to make A2A payments a feature of everyday life.

The infrastructure is largely ready. The consumer use cases aren’t

Banks across Europe have adopted the EU Instant Payments Regulation (IPR) and the 24/7 payments infrastructure is live.

So, if the technology exists, what will it take to become a go-to alternative to Visa and Mastercard?

Europeans aren’t using alternatives to the big two card companies at the checkout because the technology isn’t as convenient or widely available. Most SEPA payments happen via internet and mobile banking

The vast majority of transactions, both e-commerce and in stores, are still made with a card. No matter the method of payment – Apple Pay at a till, online check out or in-app payments – the card is the default. If it offers no advantage to the customer, why would they change their behaviour?

For the EU’s payment system to succeed, it requires three layers to work together in tandem:

- Rails (SEPA Instant): the system that enables instant payment processing across Europe

- Scheme/orchestration: these define how banks connect, payment standards, liability rules, and dispute or settlement processes

- Consumer UX & merchant acceptance: it needs to be straightforward and familiar for consumers and used by merchant POS systems

Visa and Mastercard succeed because they solve layer three. Payments are effortless for consumers, and customer experience is the biggest driver of action. It doesn’t matter to them that merchants pay interchange fees and wait 2 to 3 days for settlements, because it takes seconds to tap, get confirmation and continue with their day.

There’s an additional barrier that concerns merchants too. Despite the benefits of A2A’s instant settlement, there is no standardised system for handling disputes when something goes wrong.

What is missing to encourage merchants to move away from Visa or Mastercard are the overlay services, such as tokenization/proxy look up, dispute management, recurring payments or refunds. Introducing these features could help A2A payments rival the card giants.

Capitalising on Europe’s modern payment rails

The deadline to implement the EU mandate for sending and receiving SCT Inst payments passed on October 2025 – so have the objectives of lowering costs, improving speed, reducing dependence on non-European networks and creating a competitive payments ecosystem being met?

The answer? Partially.

SEPA Instant has been built, adopted and implemented, but consumers still aren’t onboard. So, what’s next?

Here’s what can inspire a shift among the public.

- Convenient checkout payment features: QR codes, one-click checkout or proxy lookups – straightforward layers that make A2A invisible and frictionless for the consumer. Wero is building these capabilities, but access is limited.

- E-commerce integration: Wero went live with merchant payments in Germany in late 2025 and expansion is planned through 2026. It’s a critical test whether this can compete with cards in the online checkout flow.

- Merchant Incentives: Instant settlements with no interchange fees are powerful reasons to increase adoption. Protective measures for consumers and dispute resolution are needed before they promote A2A over card payments.

- Bank Incentives: There has been heavy investment in 24/7 infrastructure, but, unlike card payments, SEPA instant doesn’t generate revenue, so banks are reluctant to fully support alternatives.

- Interoperability Across Markets: Fragmentation is still a huge challenge. Domestic solutions work seamlessly, but there is still friction when a German consumer pays a French merchant. Wero’s expansion will help, but more needs to be done.

The long walk to mainstream A2A payments

Contactless payments were launched in the UK in 2007, offering a genuinely more convenient alternative to chip and pin. The Olympics in 2012 was billed as the ‘first contactless games’ with terminals at venues and London’s transport network adopting the technology during and after the event. But change didn’t happen overnight. It took until 2018, over 10 years since its introduction, for contactless become the preferred payment method.

In 2020 we asked whether EU banks could break Visa and Mastercard’s grip. They have built the infrastructure to compete but seem to have forgotten why the regulation was introduced.

Amid growing concerns around the security of Europe’s payment systems, the EPI needs to force change by making an A2A payment as seamless as tapping a card, and they don’t have the luxury of waiting 10 years to shift consumer habits.

Want to know more?

We have decades of hands-on experience across instant and interoperable payments, from regulatory strategy and scheme participation to technical integration and operational readiness.

If you’d like to know more today, reach out to speak to our team.

Share this post

Written by

Santhosh Kumar

Senior Business Analyst, Red Compass Labs

Resources