Open all hours: G20, stablecoins and fixing cross-border payments

The global payments system is being rewired. Why? And will it happen in time?

Alright, story time.

In 2020, the world’s 20 biggest economies sat down and asked a simple question: why, in the twenty-first century, does it still cost so much to send money across borders?

Why is it slow?

Why is it opaque?

Why do you not know what fees you’re paying until it’s too late?

Out of that conversation came a set of commitments. A homework assignment for the global financial system. The G20 roadmap set out 19 building blocks for improving cross-border payments, with a hard target: by 2027, those payments should be faster, cheaper, more transparent, and more accessible.

A year later, in 2021, the G20 formally endorsed a set of quantitative targets against those four goals. The most famous one being 75% of cross-border payments should be credited within an hour by 2027. In 2022, the Financial Stability Board (FSB) published its implementation approach, outlining how progress toward those targets would be measured.

One of those building blocks, BB19, was extending the operating hours of RTGS systems, the Real-Time Gross Settlement infrastructure that sits at the heart of how central banks move money between commercial banks. This was a key focus of the G20 roadmap – by expanding the overlap with other RTGS systems, you can extend the global settlement window.

The logic is straightforward. When the Bank of England’s RTGS system (CHAPS) closes for the night, and the US Federal Reserve’s system hasn’t yet opened, there is a gap. Payments get stuck waiting for a counterpart system to open. Money doesn’t move.

Correspondent banking — the chain of intermediary banks that connects London to Delhi to New York (and so on) — gets backed up.

Extending settlement windows would shrink that gap and, in theory, make cross-border payments faster and cheaper.

A shortfall

Years go by. In October 2025, the FSB — the international body that oversees the G20 payments programme — published its annual progress report. The verdict was sobering. The FSB (Financial Stability Board) stated directly that it is “unlikely that satisfactory improvements at the global level will be achieved in line with the 2027 Roadmap timetable.”

Costs are still high. Speed has improved in some corridors but not at the global level. Hitting the 2027 targets, the FSB concluded, is increasingly out of reach.

Andrew Bailey, the Governor of the Bank of England and FSB Chair since July 2025, wrote to G20 finance ministers acknowledging the shortfall. Full, timely, and consistent implementation of G20 reforms has not been achieved, his letter warned, leaving the financial system vulnerable. Progress is being made on some fronts, but the overall picture is of a deadline slipping.

What makes this notable is that Andrew Bailey is not just the head of the FSB. He is also the governor overseeing CHAPS — the Bank of England’s own RTGS system. The man writing the letter about G20’s struggles is the same man overseeing one of the most significant steps being taken to address them.

Three central banks, one direction

So what is being done to address them?

Three of the world’s most important central banks have independently moved to extend the operating hours of their payment systems. Taken together, they tell a much bigger story than the G20 alone.

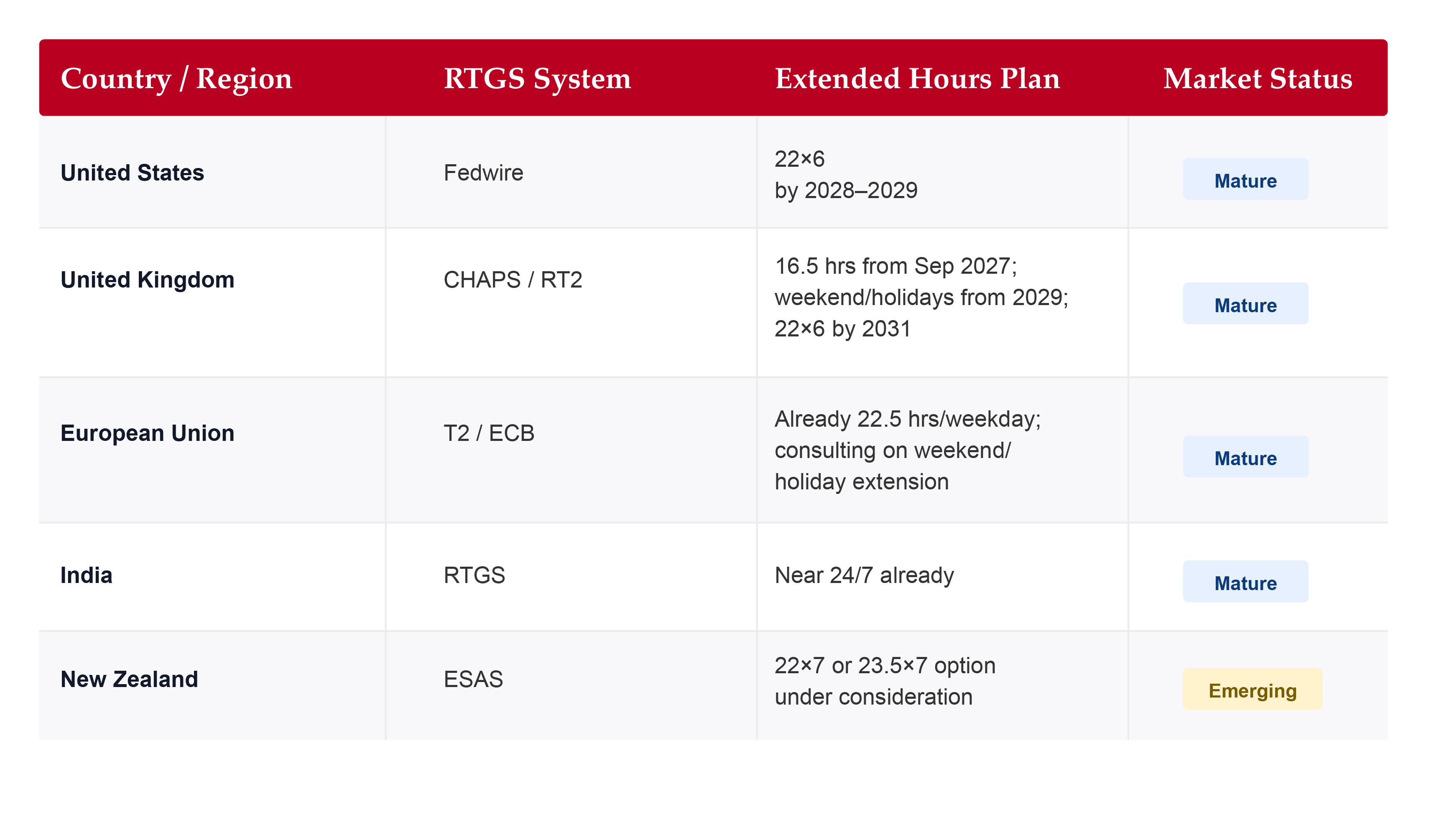

The Fedwire-Federal Reserve (United States)

In October 2025, the Federal Reserve announced it would extend Fedwire operations to a 22-hour-a-day, six-day-a-week schedule (known as 22×6) by 2028 or 2029. The Fed had initially explored a full 24/7 model but pulled back. There isn’t a big enough business case yet. Running central bank money around the clock, without commercial bank demand in the early hours, is not a productive use of the infrastructure. The 22×6 expansion is an interim step. The door is open to 22×7×365 at least two years after 22×6 is implemented.

CHAPS – Bank of England (United Kingdom)

The Bank of England’s CHAPS system, which runs on RT2 — the renewed RTGS platform launched in April 2025 — has published a phased roadmap for extending its settlement window. Today, CHAPS opens at 6am. By September 2027, it will open at 1:30am — giving the system 16.5 hours of operation, Monday to Friday. No earlier than 2029, it will add Sundays and certain bank holidays (excluding Christmas Day, New Year’s Day, and Easter Sunday). By 2031 at the earliest, the target is 22×6. And beyond that, the Bank is consulting on whether the long-term end-state should be 22×7 or 23.5×7.

T2 – European Central Bank (European Union)

The ECB’s T2 system is ahead of most peer RTGS systems globally. It already operates 22.5 hours a day on weekdays. In June 2025, the ECB launched a public consultation on extending further: primarily moving to a six or seven-day operational week, enabling settlement on Saturdays, Sundays, and holidays. No specific implementation timeline has been set; the ECB has described the consultation as an open dialogue rather than a proposal with fixed dates. The results of that consultation were published in May 2026.

When all three of these systems are operating on their extended schedules, there will be a window of around 16 hours during which the dollar, sterling, and euro settlement systems are all simultaneously open. Any payment that needs to cross between those currencies in that window will be able to clear without waiting for a system to open. That is faster. That is the G20 building block being addressed in practice.

But this isn’t really about the G20 roadmap

Here is what the headlines about CHAPS and Fedwire are not saying. The G20 deadline is the visible reason. It is not the primary one.

When the G20 program was designed in 2020, tokenized deposits barely existed as a concept. Stablecoins were a niche crypto asset. Central Bank Digital Currencies (CBDC) were in early research phases. The GENIUS Act — the US legislation that began to formalize the stablecoin framework — did not arrive until 2024.

The payments landscape has shifted fundamentally since those original targets were written. And the new landscape has a defining characteristic that the old one did not: it operates 24/7.

Stablecoins operate 24/7. Tokenized deposits operate 24/7. CBDCs, where they exist, are designed to operate 24/7. These represent the next generation of how money moves. And central banks that want their money to be usable in that ecosystem need their infrastructure to be available when that ecosystem is running.

The Bank of England has stated this explicitly. Its consultation papers describe extending settlement hours as “an important part of delivering its vision of a safe and resilient multi-money ecosystem” where tokenized deposits, stablecoins, and central bank money can coexist and interoperate. If a commercial bank wants to use central bank money to settle a tokenized deposit transaction at 2 am on a Sunday, CHAPS needs to be open.

This is an unnamed goal. No one in the original 2020 G20 roadmap wrote it down as a target because the technology didn’t exist yet. But it is the reason why the ambition goes beyond what the G20 strictly requires. It is why 22×6 is a step, not a destination. And it is why the trajectory points toward something approaching always-on.

Not everyone is moving at the same speed

For the G20 target to be met, the extended settlement window needs to exist across all the major currency corridors that cross-border payments flow through. And that is where the picture becomes more complicated.

India and New Zealand are G20 members with significant cross-border payment flows. Some are already operating near-extended hours. Others are still working towards it. The consultation processes in different jurisdictions have offered options — 22×7, or 23.5 hours a day — rather than mandates.

If the goal is to eliminate the gap between settlement windows globally, then alignment matters. A 16-hour overlap between the dollar and sterling systems helps. But if the rupee, for instance, is still unavailable for several of those hours, the correspondent banking chain is still broken at a link. The G20 target requires everyone to move, not just the largest three.

What this means

The story of CHAPS extending its hours is, on its surface, a story about a central bank updating its operating schedule to help a G20 program hit its targets. That reading is not wrong. But it is incomplete.

The deeper story is about central banks positioning themselves for a payments future that did not exist when the G20 set its homework in 2020. Stablecoins, tokenized deposits, and CBDCs are not future speculation — they are present reality, growing in scale and adoption. The infrastructure that settles them in central bank money needs to be available when they run.

Andrew Bailey sits at the intersection of both narratives. As FSB Chair, he is accountable for G20’s progress — and is candid that it is falling short. As the governor overseeing CHAPS and RT2, he is also building the infrastructure that goes beyond what the G20 asked for. The letter to G20 finance ministers and the CHAPS consultation paper are two documents from the same desk, pointing in the same direction.

The global settlement window is expanding. Not because G20 demanded it (though that helped). But because the future of money is already running 24/7, and the central bank infrastructure that underpins it needs to catch up.

Want to know more about digital assets?

Stablecoins are redefining settlement and banks need to be ready to integrate them as a settlement layer. Find out how that might look.

Share this post

Written by

Geeta Narkhede

Senior Business Analyst, RedCompass Labs

Santhosh Kumar

Senior Business Analyst, RedCompass Labs

Resources