TARGET2 & ISO 20022: What you need to know

Europe’s payment engine is taking a major step towards ISO 20022 alignment.

“A stitch in time saves nine,” goes the old saying.

Small, timely maintenance prevents larger repairs later.

When Europe launched its newly consolidated TARGET services in March 2023, the European Central Bank (ECB) deliberately froze message versions at the 2019 version of ISO 20022 (MR2019).

At the time, Europe was merging several major systems:

- T2 (TARGET2) – the core large-value payment system

- T2S (TARGET2-Securities) – securities settlement

- TIPS (TARGET Instant Payment Settlement) – instant payments

- CLM (Central Liquidity Management) – liquidity management

Introducing annual ISO updates during such a large-scale transformation would have been a nightmare for the industry.

So the ECB paused updates.

However, ISO continued to evolve. Between 2020 and 2024, five new maintenance releases were published.

At the same time, the wider payments ecosystem continued to evolve through CBPR+ (the Swift cross-border standard), HVPS+ (global high-value payment guidelines), and other market infrastructures.

As a result, T2 gradually fell out of alignment with the current ISO standard.

It now has five seams to restitch.

What parts of the TARGET2 system are affected by ISO 20022?

The ECB has activated its “unfreeze” strategy, beginning in June 2026, with an upgrade to at least ISO MR2024.

To understand the change, it helps to understand how T2 works today.

RTGS: Real-Time Gross Settlement

This is the main engine. It processes large euro payments between banks in real time, one by one.

If Bank A owes Bank B €500 million, it moves here.

It also handles customer payments.

CLM: Central Liquidity Management

This manages how banks hold and move money inside the system.

It controls main cash accounts, transfers of liquidity between systems, and intraday liquidity (money banks need during the day).

CoCo: Common Components

These are shared services used by all TARGET systems, such as reference data (central records of participants and accounts), business day calendars, and technical message headers.

The June 2026 upgrade affects all three areas, but not equally.

What is actually changing for T2 and ISO 20022 in 2026?

This is where it gets technical.

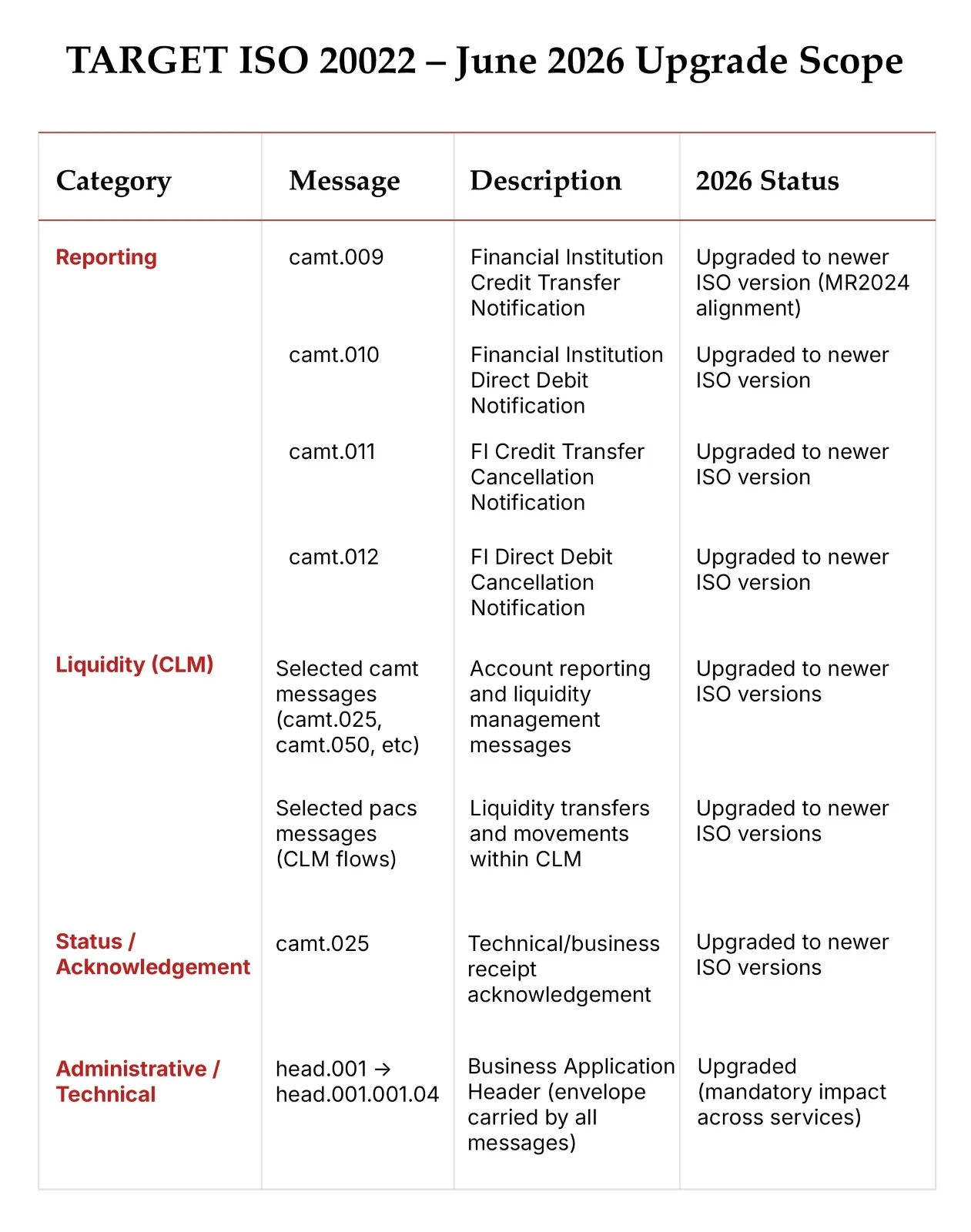

For the main payment engine (RTGS), the core payment messages (pacs messages) will stay on the old version (MR2019), intentionally.

However, supporting messages will be upgraded. These include:

- Reporting messages

- Liquidity-related messages

- Status messages

- Administrative messages

One particularly important change involves something called head.001, which is a Business Application Header in ISO 20022.

That means every message sent through RTGS will be affected, even if the payment itself looks the same. That makes it incredibly important.

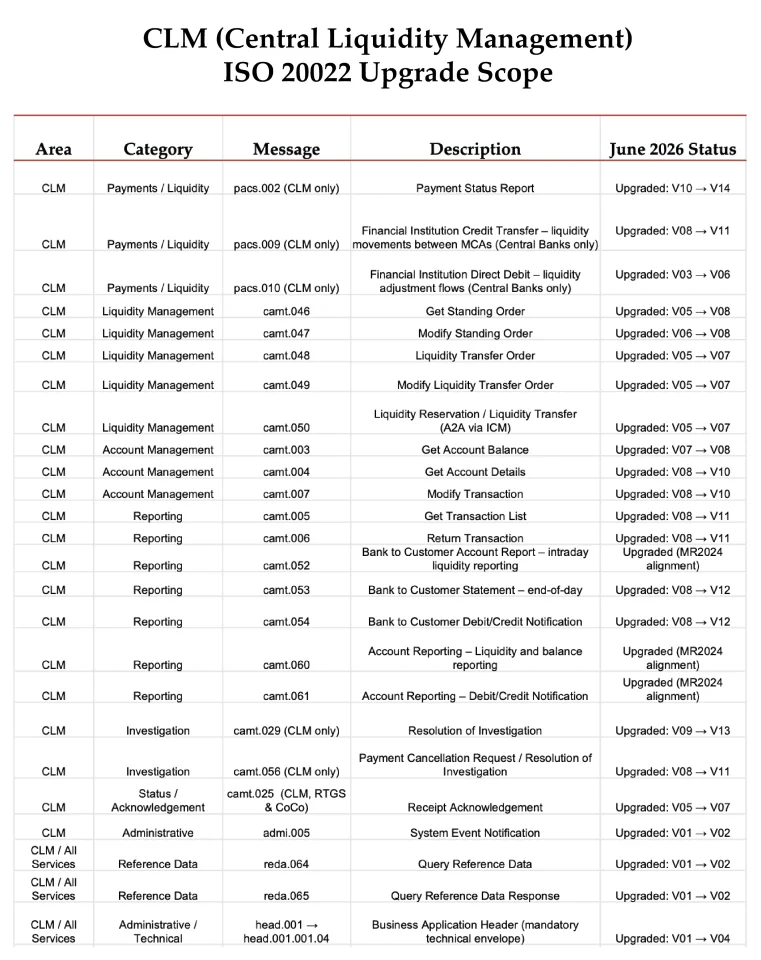

For liquidity management (CLM), more messages will move to newer ISO versions, especially:

- Liquidity transfers

- Account management

- Reporting

These changes are mainly updates to the format of the information being sent. That includes:

- New technical schema versions

Think of this like a new version of a form. The layout or labels may change slightly, but you’re still filling in the same kind of information.

- Updated data types (for example, Bank Identifier Code formats)

Some pieces of information now have to follow slightly updated rules. Like changing the way a postcode or account number is written so it fits a new standard format.

- Alignment with global standards

The goal is to make sure everyone around the world uses the same structure and rules, so systems can “talk” to each other more easily.

- Structural clean-ups

This is like tidying up a spreadsheet. It’s reorganising fields to make everything clearer and more consistent.

In short: these updates help systems stay in sync and follow common rules. They improve how the information is structured behind the scenes.

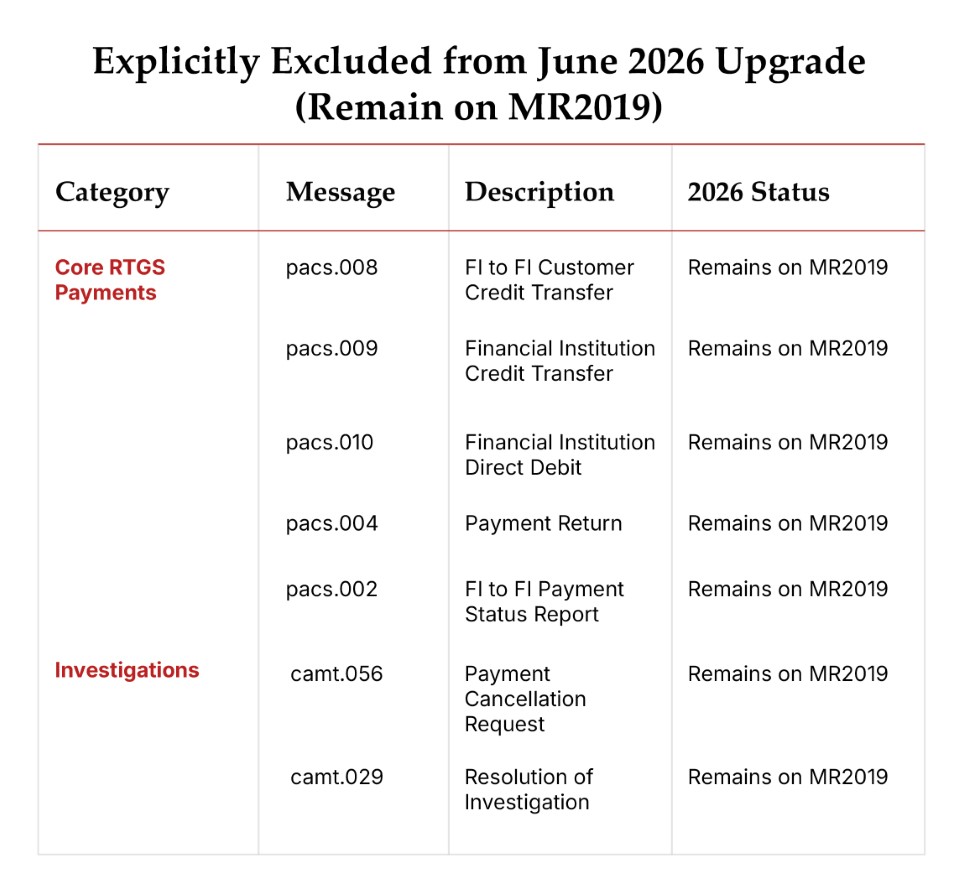

What is not changing for T2 in 2026?

This is important. In 2026, some of the most widely used RTGS payment messages will not be updated as part of the ISO 20022 transition.

These include:

- Customer credit transfers

Payments sent on behalf of customers (for example, a company making a large supplier payment).

- Financial Institution Credit Transfer

Payments banks send directly to each other.

- Payment recalls

Requests to pull back a payment that was sent in error.

- Status reports

Messages that confirm whether a payment was received, processed, rejected, or is still pending.

In plain terms: The core payment flows that move money between banks are staying structurally the same in 2026. That’s why this update is being described as technical alignment rather than a major functional change. The most critical, high-volume payment messages will not be redesigned at this stage.

So, why aren’t they changing?

Because Europe wants to stay aligned with global payment standards. Namely, the two international rulebooks for how large-value and cross-border payments should be structured:

- HVPS+, which sets guidelines for high-value domestic payments (the large payments banks send between each other).

- CBPR+, which sets guidelines for cross-border payments sent over Swift.

If Europe changed its message formats too early or too differently would have hurt interoperability. Without alignment to global ISO 20022 practice, banks would be forced to translate between competing standards — adding complexity, cost, and friction to cross-border payments that are already anything but straightforward.

So instead of moving independently, Europe is waiting for global market practice to be fully agreed upon.

The current expectations suggest these changes will take place around 2027, once global market practice is finalised.

So June 2026 is not the final alteration. More, the beginning of the catch-up process. And extra changes are likely to follow once the global position is clear.

What does this mean for you?

Even if the business outcome is the same (you’re sending the same kind of payment), the plumbing underneath is changing. And banks still have to do real work to avoid errors, delays, or rejected payments.

So, as a bank, you will need to:

- Update your systems to support new ISO versions

Payment messages are like templates. If the template changes, your systems need to be able to create and read the new version.

- Handle multiple message versions correctly

During the transition, some messages will use the old format and some the new one. You must recognise both and process them correctly. Make your code backward compatible, go live early, and use a date parameter to change XSD schemas automatically.

- Update validation rules

Banks use automated checks to confirm messages are filled in properly (right format, right fields, right lengths). Those checks must be updated to match the new rules.

- Ensure correct message headers

Each message includes “label” information that tells systems what type/version it is. If that label is wrong, the message can be routed incorrectly or rejected.

- Test thoroughly

Even small format changes can break integrations. You need end-to-end testing across internal systems and external partners.

- Be ready for the official cutover

There will be a point where the market switches over. If you’re not ready on that date, payments may fail, be delayed, or require manual fixes. That’s going to lead to unhappy customers and a lot of stress for you.

This is a technical change that can cause disruption if it isn’t treated seriously.

I’m a bank. What should I do to prepare for the TARGET2 ISO 20022 updates in 2026?

There are a number of things. You must first make your systems “version-aware” – they can no longer assume everything is MR2019. Then, update your message validation, because some data types and code lists have changed. Generate messages using the correct new header version. And ensure compatibility across system-to-system channels (Application-to-Application), user interfaces (User-to-Application, or U2A), and backup channels.

These are mandatory technical compliance upgrades, not optional enhancements. And if you need help with anything you’ve read in this article, speak to RedCompass Labs. We’re always happy to help.

Why this matters

The June 2026 release is Europe reconnecting to global ISO standards. It sets the stage for future changes. And it’s a signal that annual ISO upgrades will likely resume.

For banks that hard-coded assumptions around MR2019, this will require engineering effort.

In infrastructure, as in tailoring, small, regular stitches keep the fabric strong. June 2026 is Europe’s first stitch back toward alignment.

Are you ready for the ISO 20022 November deadlines?

Our latest research found that 44% of global banks are still behind schedule.

RedCompass Labs’ new report assesses readiness across two critical challenges: structured address migration and changes to excetions and investigations handling.

Share this post

Written by

Arun Kumar Saravanan

Senior Business Analyst, RedCompass Labs

Resources